As U.S. multi-state operators (MSOs) await federal approval of cannabis, the companies will increasingly need creative ways to finance acquisitions and growth. Curaleaf (CURLF) just announced a creative financing deal that improves liquidity and adds the potential for more financing down the road. The stock is down nearly 50% to recent lows at $6 where investors will be rewarded with major catalysts ahead of federal approval and the listings on major stock exchanges.

Cash Needs

Investors need to remember that Curaleaf is on pace to be the largest U.S. MSO and possibly the largest cannabis company in the world by revenues. Beacon Securities had predicted that 2020 revenues would top $1.12 billion and 2021 revenues at $1.60 billion.

The company ended Q1 with a cash balance of $172.6 million. As with most MSOs, Curaleaf had a small EBITDA loss of $3.7 million so the company needs cash to fund current operations and capital expenditures.

In addition, the company has deals for both the Select brand and Grassroots that had original listed market valuations of $1.8 billion. The deals have the following transaction terms:

- Select on May 1 – ~$949 million, composed of ~95.6 million shares and $200 million earnout paid in shares.

- Grassroots on July 17 – ~$875 million, composed of $75 million in cash, 102.8 million shares of Curaleaf and $40 million Curaleaf shares priced at the closing price.

The good news is that both large deals only require $75 million in cash payouts. The announced sale-leaseback of six properties in three states for $28.3 million adds a source of liquidity not previously available to the cannabis sector.

Curaleaf ended Q2 with $82 million worth of property and equipment and another $69 million in investments. These two asset piles plus acquired assets will provide more access to liquidity, if needed by the company.

Future Global Leader

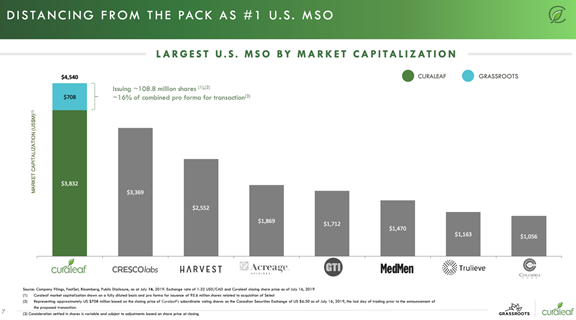

The U.S. cannabis market remains in constant flux due to most market leaders having multiple acquisitions still in flux leaving aggressive expansion plans on hold. Curaleaf provides this handy view of the market cap leaders amongst the U.S. MSOs.

(Source: Curaleaf presentation)

Curaleaf has lost all the gains since announcing the Grassroots deals. The stock will have a diluted share count of ~659 million shares once closing both deals leading to a listed market cap of only ~$4.1 billion.

The more interesting story is the March pro-forma revenues of $87 million placing Curaleaf in a position for global leadership. Remember that Canopy Growth (CGC) had June quarter revenues of C$90.5 million and Aurora Cannabis (ACB) had preliminary sales of up to C$107.0 million for only $80.6 million.

Based on these numbers, Curaleaf is already the market leader in revenues from the cannabis market.

The Consensus Verdict

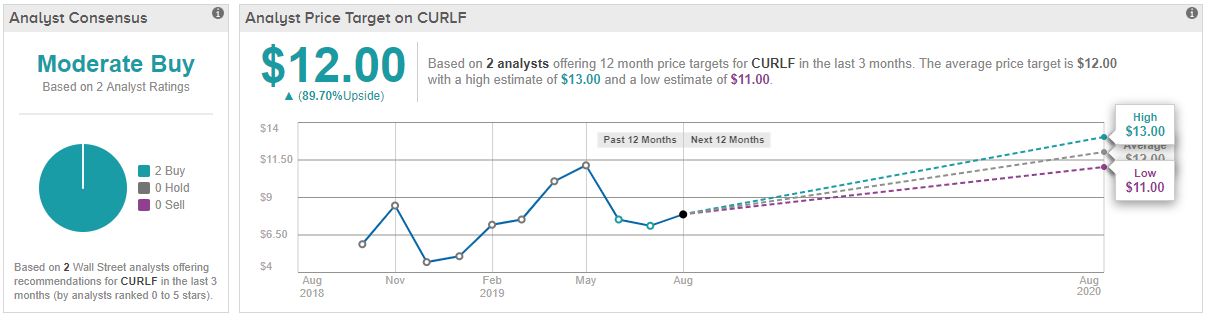

TipRanks’ data shows a small but bullish camp backing this US cannabis player. The ‘Moderate Buy’ stock has amassed 2 ‘buy’ ratings in the last three months. The 12-month average price target stands tall at $12.00, marking nearly 90% in return potential. (See Curaleaf’s price targets and analyst ratings on TipRanks)

Takeaway

The key investor takeaway is that Curaleaf is in the process of building the market leading American cannabis company. The recent June quarter results of the large Canadian LPs place the U.S. MSO in a global leadership position without even leaving the U.S. market.

The leading U.S. MSO remains a long-term buy for investors until the stock market views Curaleaf in the same light as companies like Aurora Cannabis and Canopy Growth.