Expectations for Aurora Cannabis (ACB) continue to go through the roof.

The latest catalyst occurred on Friday April 5th, 2019 where Aurora was awarded 5 of 13 tender lots in Germany where there was a public submission process for gaining access to the Germany Cannabis market. There were 79 entrants, but Aurora, along with Aphria (APHA), were awarded the highest number of tender lots among those who submitted proposals to the Germany Government for medical cannabis cultivation rights.

The stock climbed by nearly 3% following the German cultivation announcement. Some investors may have expected a bigger rally but given the limited production volumes of 1,000/Kg per year over a four-year timeframe, the German market is relatively small or nascent in comparison to North America.

The 1,000/Kg production volume is somewhat additive to revenue, as it implies 1,000,000 in additional retail gram sales at a wholesale price point of appx. $5 per gram, or $5 million in additional revenue once production reaches scale. Retail price points for cannabis hover between $8 to $10 per gram, but have trended lower in recent quarters, and because ACB is operating as a wholesaler the price point for its cannabis is likely lower on a per gram basis.

The perceived value of the German announcement might be small initially, but long-term the perceived value of the German market could be more additive to long-term financial results than initially anticipated. Laurentian Bank Securities estimates that by 2028 the German Medical market will grow to a figure of 755,556/Kg annually or 755M grams/annually, and when translated to wholesale pricing of appx. $5/gram would imply a $3.775B market opportunity annually for ACB, which is why the initial impact might be low, but the long-term narrative seems mostly positive.

Source: Laurentian Bank Securities

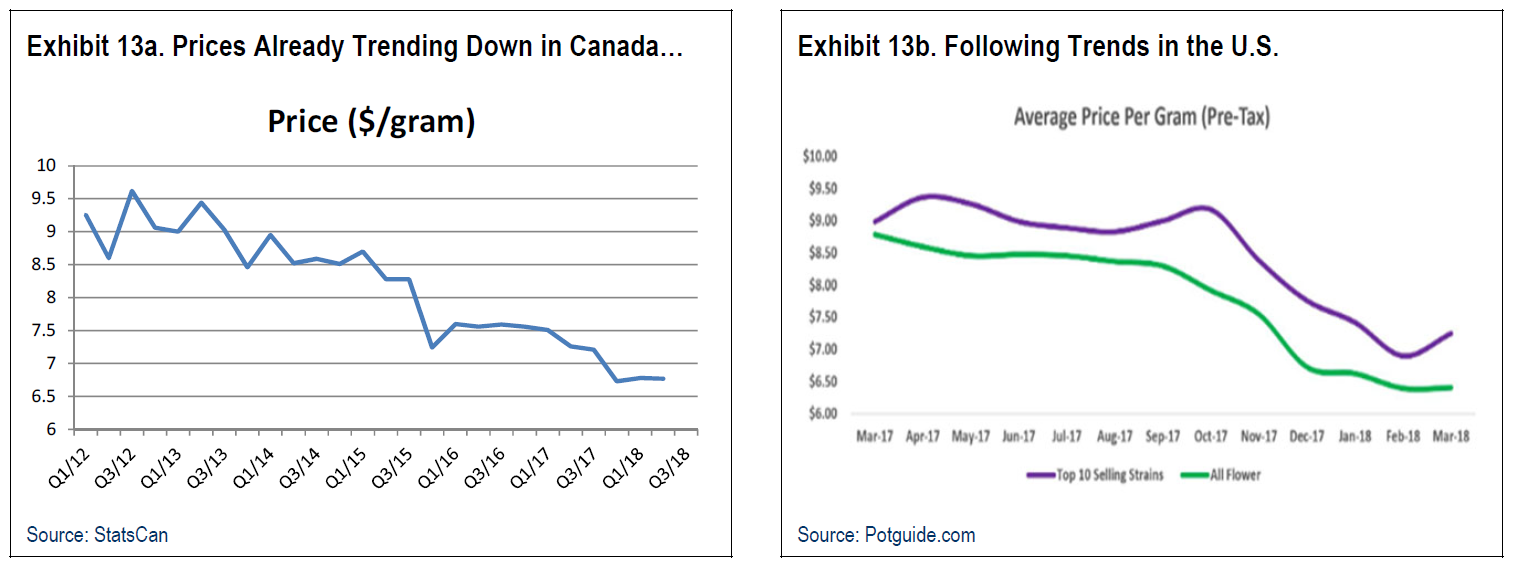

Keep in mind, the price per gram is trending lower across Canada and the United States, so expansion into other foreign markets is structural to the growth thesis. Retail pricing has trended lower to appx. $6-$7 per gram in both Canada and the United States. The pricing may continue to trend even lower, as production is expected to exceed demand in these markets, according to various reports. So, margin headwinds might diminish profitability, but then again Aurora anticipates that it can bring production cost per gram below $1 based on its own forecasts, which helps diminish the pricing headwinds as they continue to scale production across various grow facilities in both Canada and the United States.

ACB is expected to scale global production to 500,000+ Kg/year by 2020, and when weighted against its current ASPs of appx $5-$6, the business is expected to grow capacity by a factor of 5x when compared to recent production of 130,000 Kg for 2019. Assuming this production timeline holds, the business will produce 500M grams of cannabis, or $2.5 to $3 billion in annual revenue (assuming prices per gram trend to $5-$6 per gram), which helps explain the heightened market capitalization of $9.29 billion as diminished earnings/profitability (currently) are tied to production ramp but will start to balance out as they sell-in their expanded production in 2020. Analysts seem more conservative on growth outlook, as Jefferies analyst Owen Bennett forecasts a more conservative revenue ramp scenario of $1.05 Billion in FY’20.

Despite a range of scenarios, the execution is clear for ACB. There’s a number of regulatory scenarios in the United States that could be additive to the growth thesis, which we will continue to explore in future articles.

To read more on the nitty gritty of what’s going on in the rising cannabis industry, click here.

Disclosure: The author has no position in ACB.

Read more on ACB: