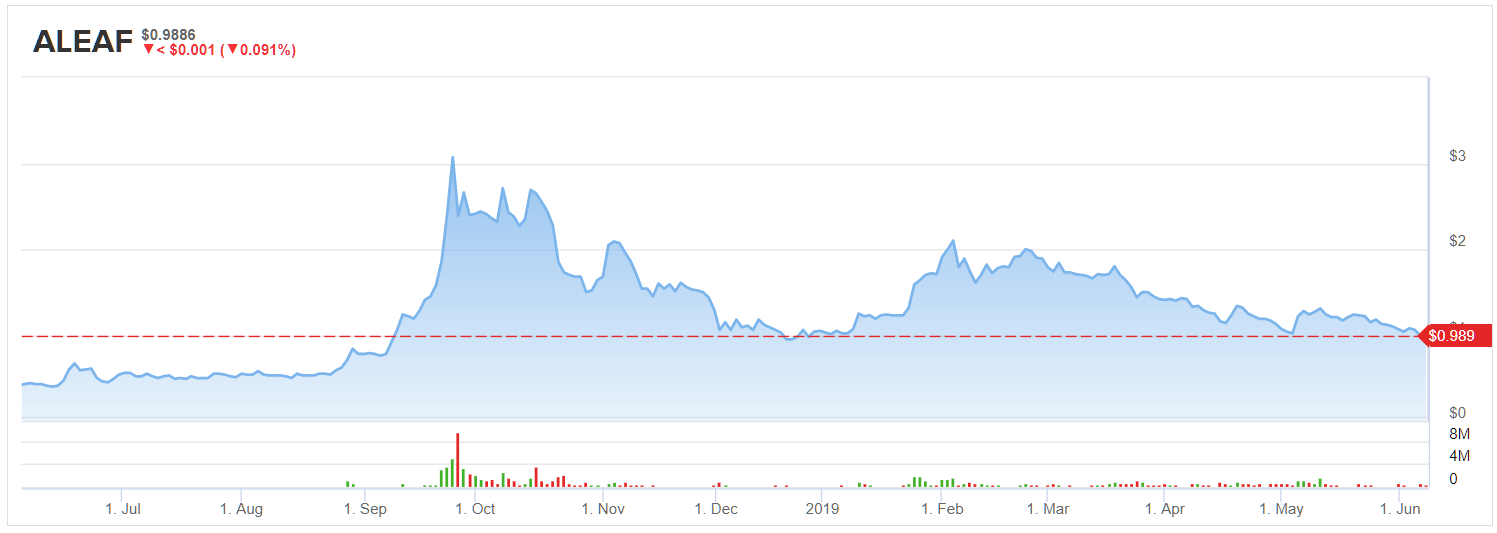

In its short history, Aleafia Health (ALEAF) has went through several periods of rapid increase in its share price, and not too long afterwards, a rapid decline in its share price.

After plunging from around $2.40 per share in the latter part of September 2018, Aleafia Health plunged to about $0.94 per share, finally finishing 2018 at close to $1.03 per share. From then until mid-February 2019, it once again jumped, this time to a double top of $1.94, before once again reversing direction, losing all its gains on the year, falling to $1.00 as I write.

With a triple bottom of about $1.00 per share since the beginning of the year, it’s apparent if Aleafia drops below the $1.00 mark, it’s almost certain to plummet below what it’s floor has been since the beginning of the year. On the other hand, if it once again manages to hold at that level, we’ll probably see it take another upward run.

The major reason for the extreme volatility in the stock, beyond being in a volatile sector at this time, is because it has yet to secure enough domestic and international supply agreements to provide a more visible, predictable performance. It also needs to complete its current expansion projects that will boost production capacity.

The Emblem deal

One of the more significant positive catalysts for Aleafia has been the acquisition of Emblem, which now combined, should be able to produce up to 138,000 kilograms annually. It also increased the number of medical clinics they control to 40, which together have served 60,000 medical patients.

On the positive side, Aleafia has quietly built itself to be one of the top-10 leaders in cannabis production. Its strong exposure to medical cannabis patients also provides it with the capability of generating wider margins than if it was solely exposed to the recreational pot market. Included in its product portfolio are sprays, capsules and oils.

What I think the market is waiting for with Aleafia is for it to prove it can effectively and efficiently scale out its operations in domestic and international markets.

Global expansion

While Aleafia has some strength in the Canadian medical cannabis market, it has been slow to make any meaningful headway in the international markets. That may change with the closing of the acquisition of Emblem.

Included with the Emblem acquisition was a joint venture with German-based Acnos Pharma GmbH, which it has a 60 percent stake in. Recently Aleafia stated it was going to leverage its supply chain network via its partnership into the German medical cannabis market. Acnos Pharma GmbH has access to 110 distribution centers and 20,000 pharmacies in the German market.

Another part of its international growth strategy is in Australia, where it closed its 10 percent equity stake in CannaPacific Pty. Limited, a licensed producer in that country.

Aleafia has been granted an import permit from the Australian Office of Drug Control, and has applied for an export permit from Health Canada. Once it receives the expected approval, the company will deliver its first shipment to an international market.

Conclusion

Aleafia Health continues to struggle because it has yet to prove it can execute on what appears to be a potentially profitable business model.

The issue of having to wait for its production facilities to be completed and for some of its permits to be approved in different markets, makes it hard for the company to retain any sustainable momentum.

Its exposure to the Canadian medical cannabis market is fairly solid, but there is enormous competition there. The company, again, has to prove it can compete against its larger competitors and peers.

Even though the company may soon export its first medical cannabis, management has said it will take about 12 to 18 months before things start to really take off on that front.

If Aleafia was saying all these things about a year ago, I would be more positive on the company, but as it stands, it does have potential, and I wouldn’t be surprised to see it enjoy another round of serious upward trajectory for its share price, but I don’t see it having anything sustainable at this time that would help it to support that level.

For that reason, I look at Aleafia as being better for a trade rather thinking in terms of taking a long-term position in the company.

It does have a clear vision and potential pathway to success, but it has yet to prove it can execute its plan. Until it does, this is going to remain a very volatile stock that could test the recent lower end of its support at about $1.03 per share.

If the company does deliver on its promises, it could enjoy a prolonged period of support on the upper end of its potential, generating nice returns for shareholders. It’ll probably take at least a year before we start to get more clarity on that potential outcome.

To read more on the nitty gritty of what’s going on in the rising cannabis industry, click here.