GW Pharmaceuticals (GWPH) has recently bounced after a solid earnings report. It also announced its phase-3 trial concerning its Epidiolex oral medicine, received positive results.

The combination of the earnings beat and forward movement of Epidiolex, provide catalysts that should continue to drive GWPH stock price higher.

The Catalysts

Revenue in the latest reporting period ended March 31, 2019 came in at $39.2 million, far above the $3 million in revenue generated in the same reporting period of 2018, beating estimates by $23.33 million.

Earnings for the quarter improved to a loss of $50.1 million, against the loss of $69.5 million year-over-year. Earnings per share was $-0.14, beating estimates by $0.07.

Cash and cash equivalents fell from $591.5 million at the end of calendar year 2018, to $521.7 million at the end of the quarter.

The second catalyst was the report of the company reaching another “primary efficacy measure with both EPIDIOLEX doses as compared to placebo.” That was the “consecutive positive Phase 3 pivotal trial for EPIDIOLEX.” The company is expected to file an sNDA in the fourth quarter of 2019.

Net sales of Epidiolex in the quarter was $33.5 million, accounting for the majority of the revenue.

Things to Consider for Current Shareholders

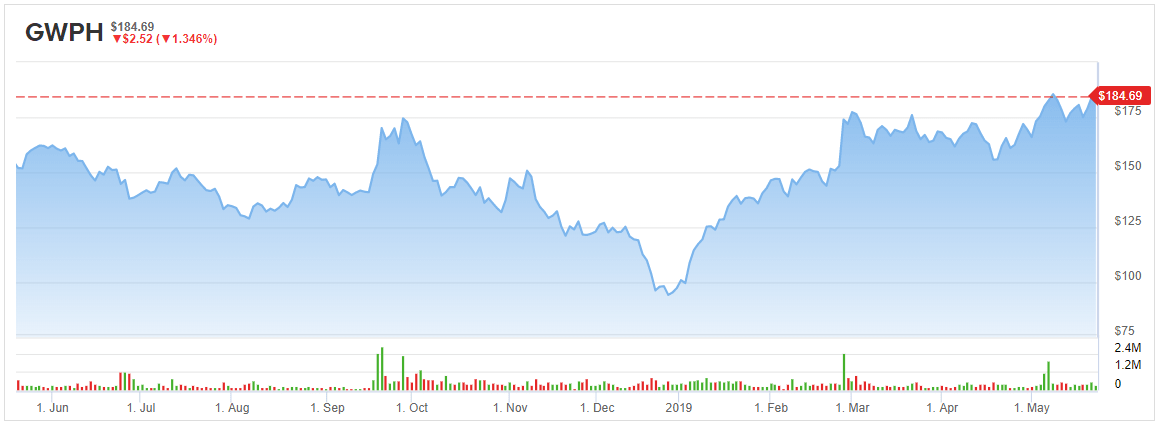

There are a couple of important things to take into consideration with existing shareholders, including its share price and whether or not it can break out from its recent new highs.

With its improvement with revenue and earnings, and its consistent positive news about Epidiolex, it would take a significant negative catalyst to reverse the sentiment in regard to the company, which suggests it may still have a lot of upward trajectory left.

For that reason, unless shareholders want to take some profits off the table, it appears to be a low-risk play to maintain a position because the share price has a lot more room to run.

Thoughts on Investors Looking to Take a Position in GWPH

Investors wanting to move quickly in and out of the stock would do better to wait to see if it drops below the recent breakout line before taking a position. Being a volatile stock, it would be best to wait for it to pull back and play the bounce if it comes.

Spending is of particular concern, as the company projected operating expenses in a range of $395 million to $425 million for full-year 2019. It’s almost certain that sales won’t be able to cover those costs.

The good news is at the end of the quarter the company had $521.7 million in cash, along with an additional $105 million it received from the sale of a review voucher in April.

Even with rapidly growing revenue, increasing insurance coverage of the treatment, and its success in clinical trials, the company will continue to struggle to generate a profit in the near term. For that reason, investors wanting a stronger risk/reward metric, will probably stay away until the company shows it can generate a profit.

One significant event that could be a powerful catalyst for GW Pharmaceuticals is if an European advisory committee gives approval this quarter for Epidiolex. If that’s how it’s plays out, patients with LGS and Dravet syndrome will have access to the treatment, providing a major boost in sales, and a quicker path to profitability; there already is pricing and reimbursement in place in key European markets Germany and France.

With all the expansion and additional costs, management believes the $521.7 million in cash and cash equivalents should be enough to cover the next 12 months.

Conclusion

GW Pharmaceuticals continues to prove it has a lot going for it, with it continuing to grow Epidiolex revenue, expand its footprint, and lowering costs while it’s doing so.

Both revenue, earnings and Epidiolex are all moving in the right direction together, and that provides a bullish scenario that should continue to support and push up the share price of the company, even though I suspect there will be a correction in the near future after its share price has almost doubled so far in 2019.

For long-term holders, it will be a chance to add more to your position and lower your cost basis.

As the company stands today, I think the long-term opportunity outweighs the short-term, because of the price support and accompanying contracting price range the company will trade in on a daily basis when it’s volatile.

If you believe in GW and are in it for the long haul, there’s really not much to do but hold on to your shares and ride the upward wave. I would be patient if you want to add to your position, waiting for the inevitable pullback.

To read more on the nitty gritty of what’s going on in the rising cannabis industry, click here.

Disclosure: The author has no positions in GWPH stock.

Read more on GWPH: