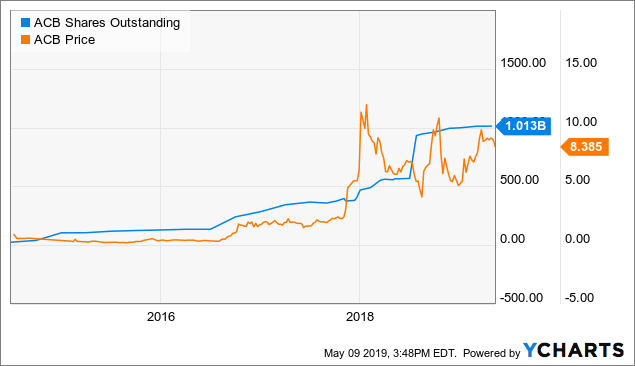

In recent years, Aurora Cannabis (ACB) has issued plenty of shares to get deals done. The CanniMed and MedReleaf deals have been major culprits in the ballooning of ACB’s share count, up from 394M at the end of 2017 to 998M at the end of 2018. There is however a saving grace to these deals beyond consolidation of the industry dominance ACB shares with Canopy Growth.

Both MedReleaf and CanniMed were preparing for a future where revenues generated from medical cannabis would continue to grow despite the legalization of recreational cannabis in Canada. While some analysts were predicting heading into legalization of recreational cannabis, that the Canadian medical cannabis market might actually shrink a little, the medical marijuana maker makers apparently didn’t agree and wanted to grab a share of the existing market. Both companies spent funds on planning and initiating clinical trials, results from which might encourage physicians allowing patients access to medical cannabis, to recommend their products in particular.

ACB’s current investor presentation has a slide at the end which lists a selection of the company’s clinical studies, of which ACB notes there are 40 underway or completed. Several of the trials listed in fact come from CanniMed or MedReleaf. For example the Cannabis Oil for Pain Effectiveness study, or COPE, is sponsored by MedReleaf and the Cannabis Extract in Refractory Epilepsy Study, or CERES, lists MedReleaf as a collaborator (apparently MedReleaf is supplying the capsules containing cannabis oil). The COPE study is expected to complete in 2019 and a positive result could see the MedReleaf product trialed become popular, potentially boosting revenues for ACB.

With regards to trials of CanniMed products, a trial of cannabis in osteoarthritis called CAPRI which tests a number of products in the CanniMed range (with varying THC:CBD ratios), is expected to complete in June 2019. Similarly a trial of CanniMed 1:20 (a product with a 1:20 ratio of THC to CBD) in children with a form of refractory epilepsy is expected to complete in 2019.

The importance of ACB showing the effectiveness of its MedReleaf and CanniMed products is increased due to the recent data suggesting sales of legal recreational cannabis in Canada are already flat, less than six months from the launch. Canadian cannabis producers can’t simply rely on the Canadian recreational market to produce the unrelenting revenue growth that is surely needed to justify their current valuations. In acquiring MedReleaf and CanniMed (among other acquisitions) ACB has increased the proportion of its revenues that come from medical cannabis and given itself an opportunity for future revenue growth from medical cannabis, reducing its dependence upon revenue growth from recreational cannabis.

ACB plans to report earnings for the quarter ending March 31, 2019, on May 14 after the bell. Given flat sales and reduced shipments facing the sector it is hard to recommend a long here, although I expect ACB to fare better than other names given its exposure to medical cannabis.

To read more on the nitty gritty of what’s going on in the rising cannabis industry, click here.

Disclosure: The author has no positions in Aurora Cannabis stock.