After cutting FY20 expectations by a substantial amount, HEXO (HEXO) has undertaken a string of capital raises in a short time frame to fund money-losing operations. Investors facing massive dilution have to question the wisdom of investing in a company with multiple equity raises with the stock plunging below $2. With the ongoing operating losses, one has to wonder whether the company won’t need to raise even more funds.

Multiple Capital Raises

Since the fateful warning on October 10, 2019, HEXO has raised ~$100 million via three capital raises.

- January 17, 2020 – $20 million via selling 11.98M shares at $1.67 per share plus warrants.

- December 26, 2019 – $25 million via selling 14.97 million shares at $1.67 plus warrants.

- October 23, 2019 – C$70 million via selling 8.0% unsecured convertible debt.

HEXO had originally forecast doubling of revenues, but the sales gains never materialized. The company had an original FY20 sales guidance of C$400 million, but analysts are now down near $60 million. The latest analyst estimates only have sales growing to top $125 million in FY21 (ending July).

Cash Burn

The problem facing HEXO and most Canadians is that sales estimates have far missed original targets. The companies spent on facilities and built up operations for a revenue base of up to double the current sales levels.

The amount of retail stores in the key provinces of Ontario and Quebec are only ~60 in mid-January. This store issue will slowly resolve over the course of 2020, but a company like HEXO needs the cash to fund growth initiatives now and can’t wait another year for a sales rebound.

In the FQ1 quarter ending October 31, HEXO ended the quarter with sales of only C$14.5 million while generating an incredibly large adjusted EBITDA loss of C$24.6 million. The loss was a slight improvement from the prior quarter, but the cannabis company remains far in the red, hence the constant capital raises when the opportunity exists.

The company even cut operating expenses during the quarter sequentially by 25%, yet total expenses were still C$35.1 million. HEXO had C$73.5 million of cash on hand at quarter end, but the company also projected spending another C$100 million on capex for the year.

Analysts don’t have HEXO reaching the quarterly sales levels to top the current expense levels for well over a year from now. The company has the additional benefit of the cannabis beverage joint venture with Molson Coors (TAP) that won’t be consolidated on the income statement, but the company needs to reduce the cash burn here before investors can focus on those benefits.

More Financings Not out of the Question, Says Analyst

Dilution will continue to be an issue for investors as the company continues to sort itself out. Desjardins analyst John Chu opined, “Following an C $800m base shelf prospectus in November 2018, we could see more financings going forward. HEXO recognizes the cannabis environment has changed dramatically and access to capital has become very difficult. Consequently, if investors are willing to invest meaningfully in the company at terms it finds acceptable, the company will consider it. HEXO also indicated to us that its ATM should commence around January 22, 2020 (recall that Aurora had raised ~C$165m through its ATM in ~4–5 months).”

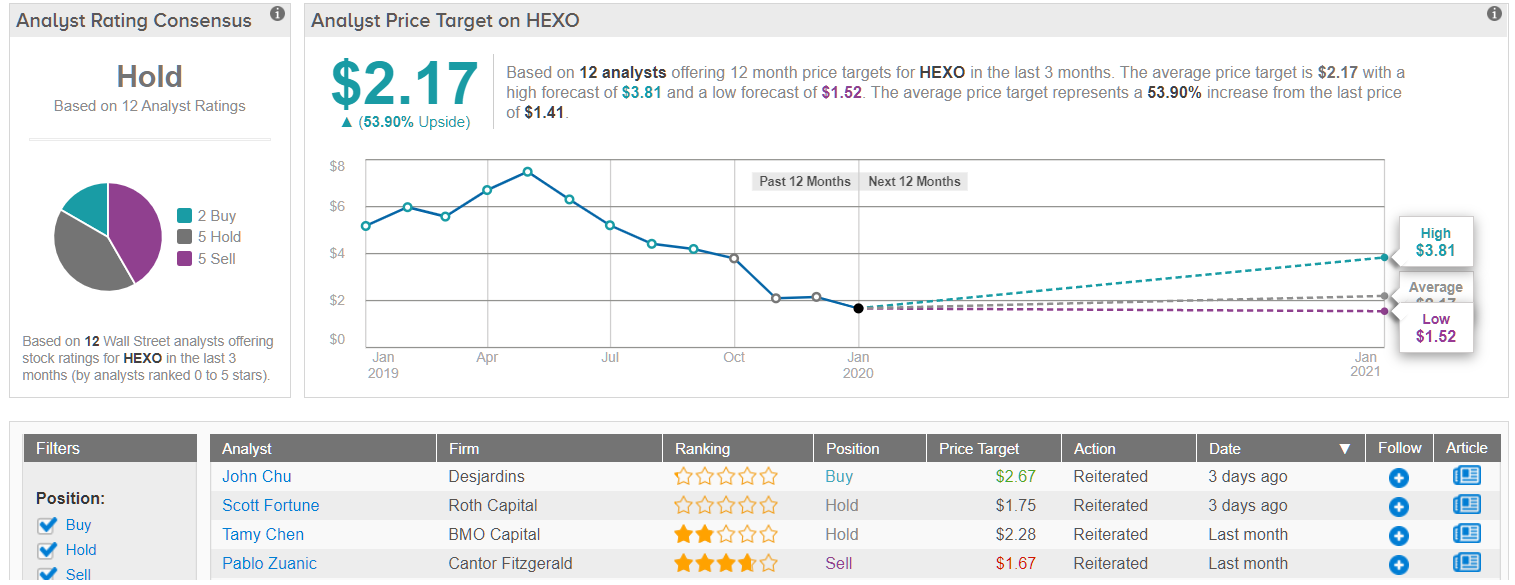

Overall, Wall Street is not convinced that HEXO is worth the risk. Based on 12 analysts tracked by TipRanks in the last 3 months, only 2 say Buy, 5 say Hold, and 5 recommend Sell. However, the 12-month average price target stands at $2.17, marking over 50% upside from where the stock is currently trading. (See HEXO stock analysis on TipRanks)

Takeaway

The key investor takeaway is that HEXO has a lot of positive catalysts to play out in 2020, but the company needs to reorganize the firm to reduce operating expenses following delayed catalysts this year. The stock had seen a recent boost due to some over excitement about the rebound in sales at competitor Organigram, but investors should be cautioned that the revenue beat was due to low quality sales.

HEXO is likely headed to new lows now as too many questions exist on whether all of these capital raises are enough to fund ongoing operating losses.

To find better ideas for cannabis stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.