As the calendar turns to November, investors can start looking forward to the September quarter earnings season for Canadian cannabis stocks. The prime focus in the next couple of weeks is whether Canopy Growth (CGC) can survive signs of pricing pressure in the sector while improving margins. The market will really hone into whether the cannabis leader can drastically improve margins while cutting costs. The stock is more attractive down at the 52-week lows around $20, but the company still needs to pair back investments to ultimately reward shareholders in the near term.

Focus on Margins

The most absurd number produced by Canopy Growth is the incredibly low gross margins. The market should highly question why the company is aggressively pursuing markets that are generating low margins.

For FQ1 ended in June, Canopy Growth generated a miniscule gross margin of 15% for a gross profit of only C$14 million. The company forecasts goals of achieving 40% gross margins that definitely changes the financial equation, but the number is still relatively small.

Top competitor Aurora Cannabis (ACB) already generates gross margins in the mid-50% range. When Canopy Growth reports FQ2 earnings tentatively on November 14, the market will want to see sequential improvements and likely a surprise jump to the 25% range.

This is the first quarter since the exit of founding CEO Bruce Linton. The market will want to see if the company can fundamentally shift spending habits with new leadership. The fear is that an external CEO is needed before the company can actually pivot to build a profitable business with large margins versus one attempting overly ambitious global scale on low margins.

The company has quarterly operating expenses in the C$116 million range. The numbers aren’t as much out of line with the global ambitions, but the level of expenses doesn’t jive with low gross margins.

The FQ2 expectations is for revenues of $85 million or C$112 million. As an example of the issue here, Canopy Growth needs to achieve quarterly revenues of C$300 million with 40% gross margins to cover this level of operating expenses.

Slow the Cash Burn

Canopy Growth ended June with a cash balance of C$3.1 billion. The company blew through C$1.4 billion in the quarter due to a combination of acquisitions, facility buildouts and operating losses.

Going forward, Canopy Growth can avoid the acquisitions that accounted for nearly C$1 billion worth of expenses. The large cannabis company still spent over C$300 million during the quarter on funding a C$92 million EBITDA loss for operations and spending C$212 million on expanding infrastructure for future growth.

The market needs to see Canopy Growth push this spending combination towards breakeven sooner rather than later.

Wall Street Verdict

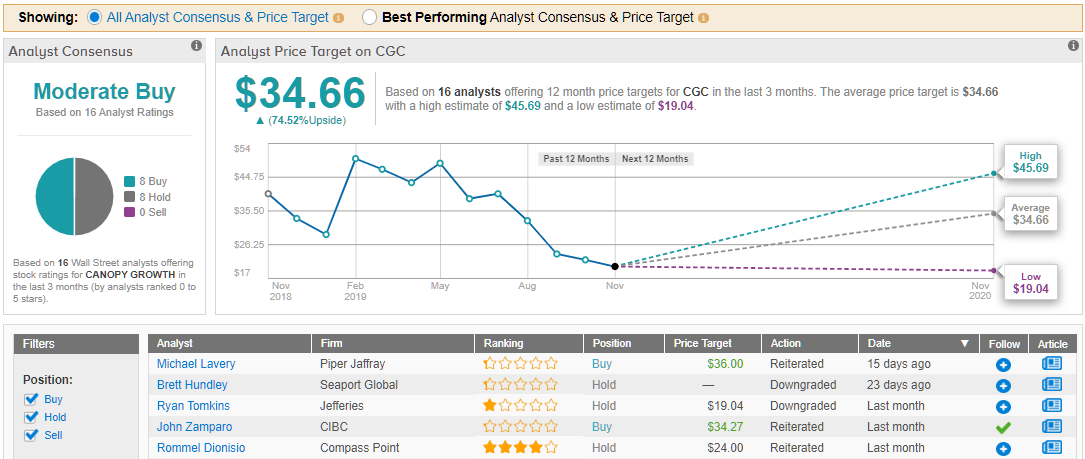

Wall Street is torn when it comes to whether to sing this cannabis giant’s praises or assess with an apprehensive gaze, as according to TipRanks, out of 8 analysts polled in the past 3 months, half are bullish on CGC stock while half remain sidelined. However, according to these analysts, the average 12-month price target for the stock stands at $34.66, which implies about 75% upside from where shares last closed. (See Canopy stock analysis on TipRanks)

Takeaway

The key investor takeaway is that Canopy Growth still needs to offer up plans to reign in global expansion plans to focus on areas where the company can generate strong cash flows. The focus needs to shift from outlining cannabis harvest growth to detailing how the company can generate profitable growth over time.

The stock has an enterprise value of $4.5 billion with FY21 sales goals of only $850 million. The value is highly questionable for a money losing stock, but Canopy Growth can change the equation with a clear path to cutting the cash burn, therefore, turning the cash balance to a war chest from a piggy bank to fund loses.

Visit TipRanks’ Trending Stocks page, and find out what companies Wall Street’s top analysts are looking at now.