As the Canadian cannabis stocks collapse, the most attractive ones to hold are the stocks with the best balance sheets to survive the downturn. Canopy Growth (CGC) falls squarely into this category with a large cash balance from the Constellation Brands (STZ) investment. The stock is more attractive down at the 52-week lows around $20, but the company continues to invest too widely in Europe to reward shareholders.

European Push

While Monday saw a lot of cannabis stocks dip, Canopy Growth saw a small bump from encouraging license and contract news in Europe. The company got a UK license for a storage and distribution facility dedicated to medical cannabis and along with a contract in Luxembourg.

Their Spectrum Therapeutics division has been in the UK for under 12 months and this move allows them to import medical cannabis from Canopy Growth facilities around the globe versus relying on third-party distributors. The move should help margins while lowering costs.

In Luxembourg, Spectrum Therapeutics has become the exclusive supplier of the Grand Duchy of Luxembourg. The contract locks in Canopy Growth as the supplier until December 31, 2021.

The biggest question remains why Canopy Growth is even chasing the business in Luxembourg where the population in the country is only 600,000. Even worse, the country only allows medical cannabis for severe unmet needs.

The market potential here clearly brings major questions to the viability of the work and why the global company is spending over C$100 million in quarterly operating expenses on revenues only generating 15% in gross margins. Even the forecast of jumping to 40% gross margins will bring up questions of whether key resources are correctly being thrown at areas where revenue potential is relatively small.

International Financials

Investors only need to review the FQ1 financials to question the big push into Europe when such a large opportunity existed in the US along with Canada. For the quarter, Canopy Growth generated C$10.5 million in revenues in comparison to a business with C$90.5 million in total quarterly revenue while dropping the ball on the US opportunity.

The majority of the international sales come from the recently closed acquisition of Germany’s C3 Cannabinoid Compound Company. At the time of the deal announcement in May, C3 supplied 19,500 patients in Germany and generated 2018 sales of C$41.5 million. All of the other European news had only generated a few million in quarterly revenues.

Part of the deal here is that the cash balance dipped to C$3.1 billion in the quarter due to the purchase of C3 and This Works to build up the European business along with the Acreage Holdings (ACRGF) call option for the US. These acquisitions have buoyed the revenue targets, but neither has helped the financials as the company is focused on vast operations around the globe where the company is chasing business in a small country like Luxembourg that can’t ever possibly generate strong margins or material profits for a Canadian company.

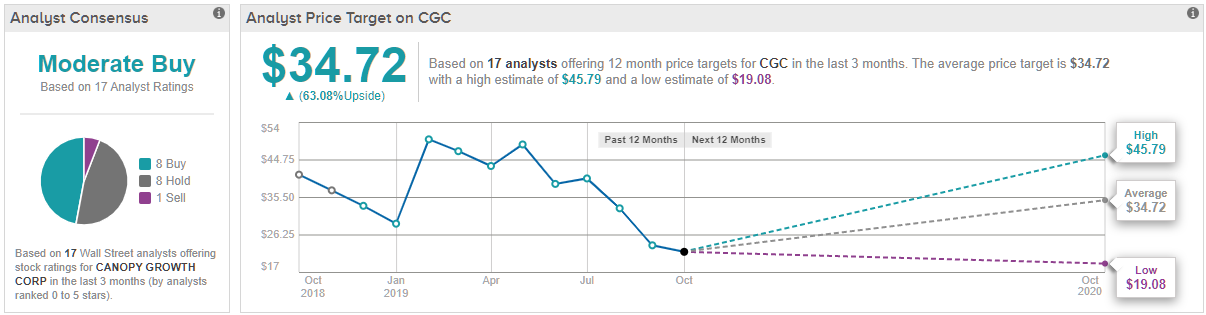

Consensus Verdict

TipRanks suggests the cautious analysts almost match up against the bulls rooting for Canopy’s opportunity. Out of 17 analysts polled in the last 3 months, 8 are bullish on CGC stock, 8 remain sidelined and one is bearish. However, with a return potential of over 60%, the stock’s consensus price target stands at $34.72. In other words, optimists still win out in the bigger picture. (See Canopy stock analysis on TipRanks)

Takeaway

The key investor takeaway is that Canopy Growth needs to reign in global expansion plans to focus on areas where the company can generate strong cash flows. This updated European news suggests the firing of the founding CEO hasn’t changed the global ambitions at all cost’s mentality of the business.

The stock is more appealing at $20, but Canopy Growth still needs to rationalize operations and production before the stock becomes a buy.

To find good ideas for cannabis stocks trading at fair value or better, visit TipRanks’ Best Stocks to Buy, a newly launched feature that unites all of TipRanks’ equity insights.

Disclosure: No position.