The original investor hope surrounding the regulatory issues at CannTrust Holdings (NYSE:CTST) was a quick solution that got the company back into business selling cannabis. The problem all along was that the news continuously got worst for the company. The final straw is the suspension of their license to produce and sell cannabis by Health Canada.

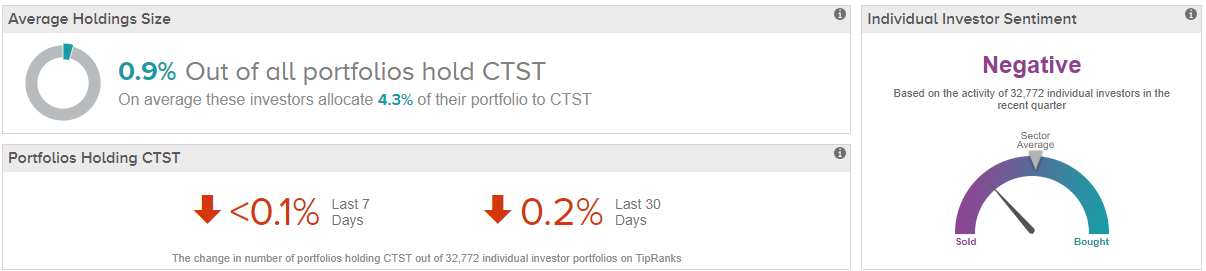

As a result, investor sentiment is negative, with individual portfolios in the TipRanks database showing a net pullback from CTST.

Not Much Left

Back on July 8, CannTrust announced that Health Canada found the Canadian cannabis company to be in non-compliance with an audit conducted by the regulatory body. Specifically, the company and executive management team had hidden the growing of cannabis in non-licensed rooms.

Originally, CannTrust presented the idea that Health Canada would rule on tests of the cannabis from these unlicensed sources within 10 to 12 business days or somewhere around mid-July. The reality is that the Canadian regulatory body only now ruled on September 17 to pull the license of CannTrust.The company reported this morning the receipt of a Notice of License Suspension under section 64(1) of the Cannabis Act (Canada). CannTrust is not allowed to produce or sell cannabis while the license is suspended. The only allowed operations are the cultivating and harvesting of existing plants in the ground.

The company had already fired the CEO and withheld sales and shipment of cannabis products while awaiting the Health Canada review. CannTrust hasn’t sold products going on three months leading to massive ongoing losses with no clear path to returning to business anytime soon, if ever.

Mounting Costs

For Q1, CannTrust had operating costs of about C$10 million in the quarter before counting C$2.2 million in selling and shipping costs. The company will incur most of these costs going forward before cutting employees.

This amount doesn’t factor in expected growth in the employee base for Q2 since CannTrust hasn’t reported the June quarter results yet. In addition, the cannabis company had about C$9.1 million in production costs for the March quarter that will be occurred in the current quarter with the company still growing cannabis in the anticipation of obtaining Health Canada approval to return to selling product.

The company burned C$19.0 million in cash during the March quarter and one can easily see those amounts repeated and exceeded in both Q2 and Q3. The good news is that the company raised $170 million back before the regulatory issues to supplement about $30 million on the balance sheet at the end of March. The company has the cash to fund these ongoing losses for an extended period.

A big worry is that shareholder lawsuits could wipe out the remaining cash. In addition, what made the stock appealing was the additional capacity expected to come online considering the move to beat the market to growing cannabis outdoor. CannTrust has lost the first mover advantage here.

Consensus Verdict

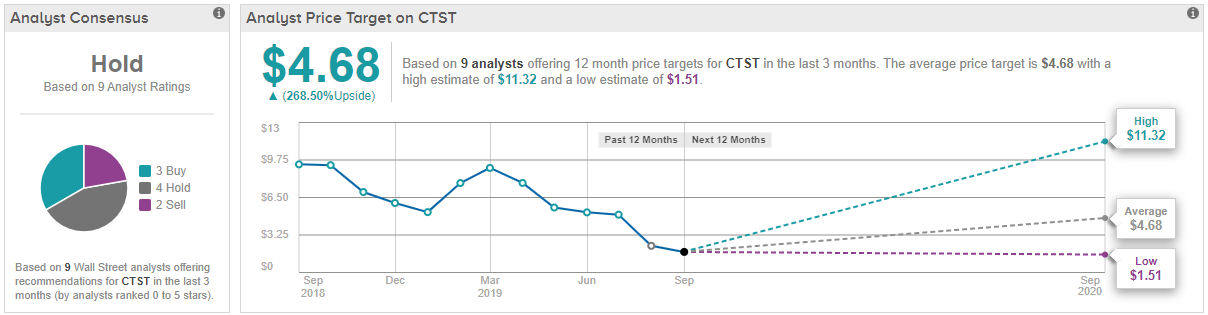

Ultimately, the word on the Street points to a sidelined majority on CannTrust. In the last three months, the embattled cannabis stock has landed 3 ‘buy’ ratings vs. 4 ‘hold’ and 2 ‘sell’ ratings. (See CTST’s price targets and analyst ratings on TipRanks)

Takeaway

The key investor takeaway is that once CannTrust failed the Health Canada audit, the stock was placed on a watch list due to intriguing value if the company was able to quickly regain compliance. The problem all along was the uncertainty surrounding the real details of the audit failure and how the regulatory body would actually act.

The best outcome here is a likely sale of the company or the cannabis production assets, but any investor is gambling to expect gains from the current stock price near $1.25. Any deal could easily be a take under considering the operating losses and legal uncertainties.

Disclosure: No position.