Aurora Cannabis (ACB) stock took a beating since the latest earnings report, when it announced a 24 percent decline in net revenue sequentially, which included a 33 percent drop in Canadian recreational pot sales. Its market-leading gross margins and cost per gram of under C$1.00 weren’t enough to support its share price.

Consequently, the company announced it would stop construction at two facilities which will save it approximately C$190 million. It also took steps to reduce the amount of its convertible debentures coming due in 2020.

While the company will continue to face short-term challenges, it’s still one of the strongest positioned Canadian-based cannabis companies to take advantage of the long-term cannabis trend that is still in the early stages of growth.

Long-Term Catalysts and Benefits to Reap

The two major catalysts for Aurora are the inevitable and significant increase in retail cannabis stores in Canada, and the impact derivative products will have on its top and bottom lines. Derivatives will be allowed to be sold in Canada in the last couple of weeks of December.

Concerning the small number of retail cannabis stores, that has come from the slow approval rate of licenses in Canada. How quickly they are approved and the new stores are opened will determine the impact on Aurora’s revenue and earnings.

A key thing to understand there, beyond the obvious lack of places to sell cannabis out of, is that it also keeps the black market strong. That’s relevant because it allows for lower-priced pot to compete against the higher-priced pot of legal competitors. That will change as the number of stores continue to climb.

On the derivatives side of the business, it will provide Aurora with the opportunity to expand its already popular portfolio of brands into higher price products that include wider margins and stronger earnings.

It’s difficult to know how quickly this’ll have an impact on Aurora because of the lack of visibility on how rapidly the company will roll out products, and how quickly they’ll be embraced by the market.

I see it having at minimum a decent impact on the performance of Aurora in the first calendar quarter of 2020, and probably giving a much clearer look at what it will mean for Aurora in the second calendar quarter of 2020, when the company should have close to a full array of derivative products offered to the market.

In the short term, the pace of opening of new retail cannabis stores will determine the growth trajectory of Aurora.

Taken together, the increase in cannabis stores and new product lines should have a meaningful impact on the performance of Aurora by the end of the second calendar quarter of 2020.

The good news is as this catalysts start to mature, Aurora has more than enough production capacity to meet growing demand.

Consensus Verdict

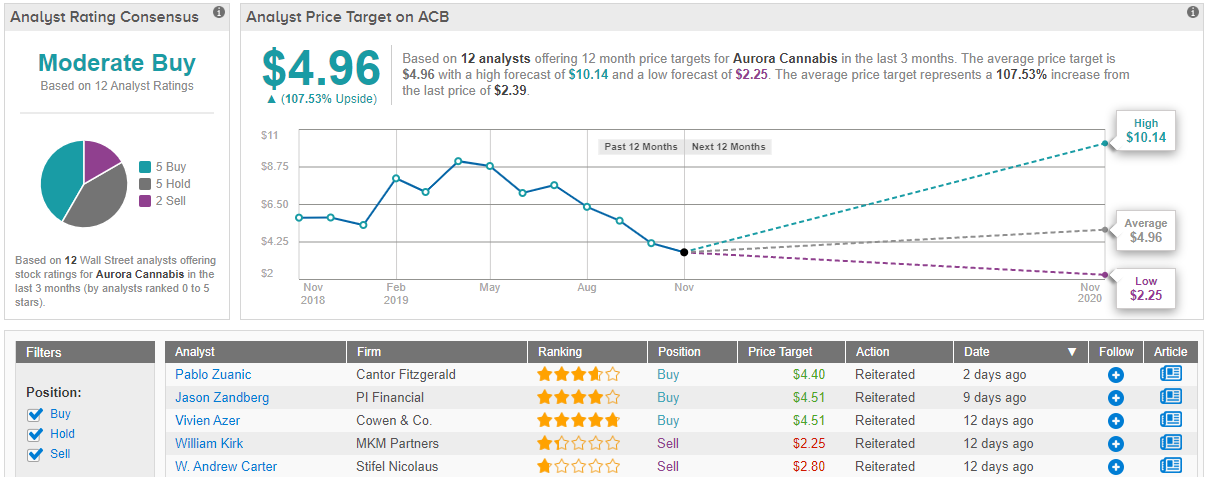

Wall Street is not convinced just yet on the Canadian weed giant, but cautious optimism is circling, as TipRanks analytics demonstrate Aurora as a Moderate Buy. Based on 12 analysts tracked in the last 3 months, 5 are bullish on ACB, 5 remain sidelined, and 2 are bearish. Importantly, the 12-month average price target stands tall at $4.96, marking over 100% upside from where the stock is currently trading. (See Aurora’s price targets and analyst ratings on TipRanks)

Conclusion

I don’t see Aurora Cannabis having another earnings disaster as it did in the last reporting period. That doesn’t mean its share price couldn’t fall further, only that the numbers have nowhere to go but up.

Only a disastrous incremental roll out of cannabis stores in Canada could keep the company from vastly improving sales in the quarters ahead. I don’t include the final calendar quarter of 2019 among those quarters. The reason why is there doesn’t seem to be a sense of urgency in Canada to expedite the licensing process.

If there is any surprise on the positive side in the last quarter of 2019, it could surprise to the upside. I wouldn’t count on it in the near term though.

Over the long term I still see Aurora Cannabis being the top company in the sector. It has unrivaled international presence, superior production capacity for long-term growth, extremely low cost per gram, and the industry leader in gross margin. These will all become key factors in the months and years ahead.

Investing in Aurora isn’t for the faint of heart, and it should be considered a long-term play with enormous upside potential. It’s not a stock to bet the farm on, but one that should be part of the portfolio allocated to growth.

I maintain that patient investors are going to be rewarded significantly. We shouldn’t focus on any one or two quarters, but the underlying fundamentals of the cannabis trend and Aurora.

To find good ideas for cannabis stocks trading at fair value or better, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.