Aurora Cannabis (ACB) is the top cannabis company in the world in my opinion, although admittedly, it’s a difficult company to value because of its decision to go a different route than its competitors, and the growing number of pieces in its overall puzzle that results in a complexity that is difficult to analyze.

By complexity I don’t mean it’s difficult to understand the individual pieces, only as mentioned above, that gathering the vast number of pieces of the company at all its points is hard to put your head around. That has created some uncertainty in the minds of some investors in my view, and that has partially held back the share price from moving a lot higher than it now stands.

Another reason hasn’t taken off like it deserves is because of the perceived need by many in the market for it to receive a big cash infusion from a large company outside of the sector. That doesn’t fit the business model or culture of Aurora in any way, and I believe it would be a disaster for it to give up control of the board and the way it operates for a temporary boost in its share price that would take what makes the company unique and compelling over the long term.

Most of those harping on the cash infusion are older investors that only acknowledge a few ways to do business. That’s why so many millennials are attracted to Aurora and many older investors aren’t.

As Aurora adviser Nelson Pelz noted, with Aurora very near to generating positive EBITDA, it wouldn’t make sense to pursue a cash infusion at the expense of giving up control of the company.

Its obvious and not so obvious value

I want to start with the most obvious strength of Aurora, and that is its market-leading production capacity, which within a couple of quarters will surge to about 625,000 kilograms.

Even here I’ve seen some commentators view this as a negative, as if having a large amount of products is somehow a negative for the company. The essential assumption is having that much cannabis is going to result in the company having no outlets to sell some of it to because of supply exceeding demand.

The good news there is the company isn’t primarily focusing on dried flower, and will take an increasing amount of its cannabis for extraction and turning it into other higher-margin products. It of course also has the largest global presence in the cannabis sector, and will have those markets as outlets to sell its product to.

Another hidden value is the flexibility it offers for Aurora from quarter to quarter as it sells or holds back distribution of its cannabis in order to obtain the best deals or ensure it has enough for specific segments of the market.

For example, in the latest reporting period the company stated it held back selling more into the recreational pot market in Canada in order to have enough to serve its medical cannabis customers.

One of the more important things investors need to understand about Aurora is it considers itself a medical cannabis company first and foremost, even though it will sell into the recreational segment to generate revenue while it’s expanding its medical cannabis business.

Another value of production capacity is it attracts interest from governments because it provides a reliable and high-quality source of cannabis that their citizens can rely upon. This is one of the reasons it has been able to secure exclusive supply contracts with countries like Australia, Brazil, Germany and Italy, among others. That is an underrated competitive advantage that will pay off in the long term.

As it’s easy to see, having a lot of production capacity is more than simply loading up on cannabis for the purpose of bragging rights, as the market will find out in the near future with Aurora.

Powerful brands and strains

Aurora has a powerful portfolio of brands, including the popular CanniMed and MedReleaf, but its brands and strains go far beyond those two well-known names.

For example, not too long ago Aurora added Hempco Food and Fiber and Chemi Pharmaceutical to its growing brand portfolio, and also has a number of pharmaceutical partnerships with companies like PharmaChoice, Pharmasave, and Shoppers Drug Mart.

It also has some of the top strains sold in Canada.

As for Hempco, it increases its exposure to hemp, adding to its other hemp brand Planet Hemp and Praise. Along with the usual hemp products, these brands also sell to the specialty markets; including kosher, certified organic, and vegan products, among others.

In the case of Chemi Pharmaceutical, it bolsters the already formidable research and development team of Aurora, adding expertise in a variety of medical applications and skin products.

The research and scientific teams at Aurora are second to none, and over the long haul will roll out products that have pricing power and solid margins.

Most recently it entered into a partnership with the UFC, where scientists from Aurora and those from the UFC will work together to find research-backed solutions to a number of conditions associated with sports, and over time, develop products that treat those conditions, eventually leveraging them across the entire sports complex, and ultimately, to the general population.

All of this and more will generate numerous popular brands for Aurora, which will continue to differentiate it from its competitors.

It has a number in place now, and will without a doubt continue to develop popular brands and strains in the future. These brands, and research and development are tied together, and they aren’t obvious to the market as to their long-term value to the company.

Conclusion

I’ve only touched on a few of the things that are part of the hidden value many investors aren’t aware of or don’t appreciate or value in the way they deserve to be.

Considering its market-leading production capacity that will widen further in the next half year or so, and the accompanying flexibility that comes with it; the numerous supply deals it has in place in Canada and foreign markets, the popular brands and strains of the company, and a research and development team that is probably the best in the business, and it’s easy to see that Aurora Cannabis is in the early stages of reaching its full potential.

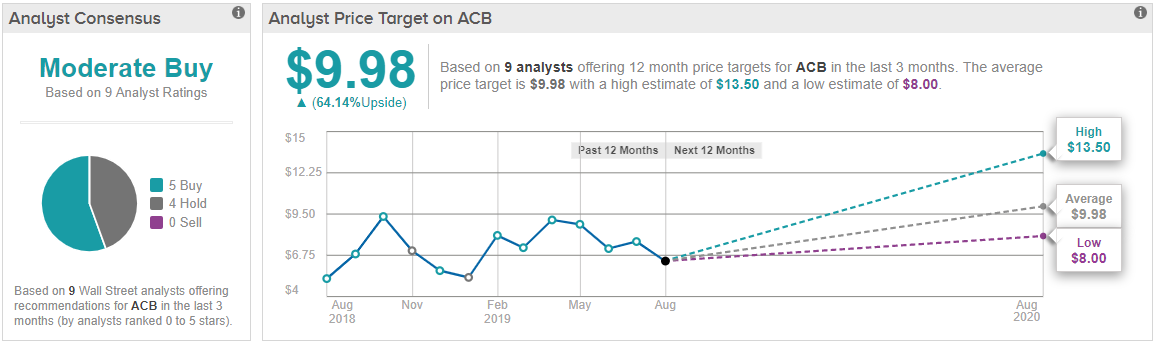

ACB has an optimistic Moderate Buy consensus rating from the Street. This breaks down into 5 ‘buy’ and 4 ‘hold’ ratings in the last three months. We can also see from TipRanks that the average analyst price target is $9.98 – 64% upside from the current share price. (See ACB’s price targets and analyst ratings on TipRanks)

Disclosure: The author has a long position in Aurora stock.