When Aphria (APHA) reports FQ2 results on January 14, the market is only hoping for sequentially stable revenues from the Canadian cannabis LP. The key to the earnings report is for the company to maintain strong financial targets for the fiscal year ending in May. How the company navigates the market over the next few months before several catalysts kick in my midyear is crucial.

Sequential Flat Revenues

The Canadian cannabis investor probably never thought one would want a company to report sequentially stable quarterly revenues. Unfortunately, an investor hopes for no more than flat revenues for the quarter ending November.

For FQ1, Aphria generated net revenues of C$126 million. The company only had net cannabis revenue of C$31 million with the majority of revenue coming from a low margin distribution business in Germany.

With Canadian cannabis sales up only slightly over the last few months, investors can’t expect much in the way in upside sales from Aphria. The average analyst estimate has sales growly slightly to C$128 million with a big jump to C$143 million for FQ3.

The problem here is that Aphria has projected annual revenues of C$650 million to C$700 million. The lack of revenue growth in the November quarter makes this estimate nearly impossible to reach.

The company comes up nearly C$100 million short on this path. The guidance for FY20 adjusted EBITDA of C$90 million provided large hopes for investors that a Canadian cannabis company can generate strong financial results, but investors might end up disappointed here without the revenue growth materializing.

Big 2020 Catalysts

A lot of the revenue issues are short term in nature. The big issue facing the Canadian LPs are the timing of 2020 catalysts.

New Ontario stores won’t open until April at the earliest and only 25 stores per month afterwards. In addition, Cannabis 2.0 products have had slow rollouts with several key provinces blocking vape sales and the lack of sales outlets in the biggest province.

The point here is that these key catalysts for 2020 are both being pushed out towards midyear, which is right after the fiscal year end for Aphria. The possibility of a guidance cut while maintaining strong FY21 estimates is very likely.

The new Diamond One facility should push product onto the market in March. Aphria will have to gain market share during the FQ4 quarter that ends in May for revenues to surge. The real upside from all of these catalysts isn’t likely until the August quarter.

Consensus Verdict

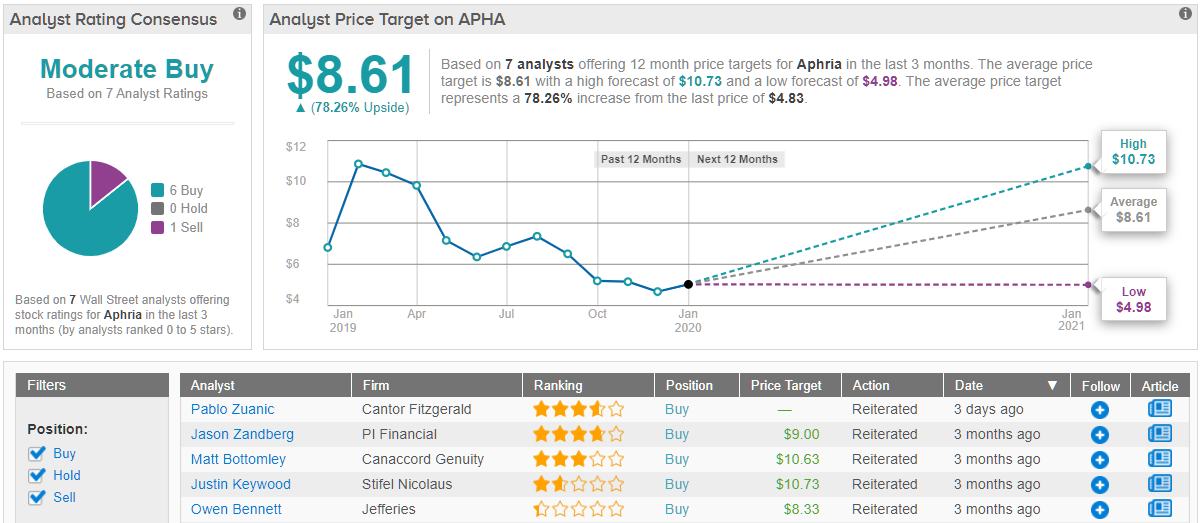

Most analysts on Wall Streets are out rooting for this cannabis stock to be a winning stock pick. Based on 7 analysts polled by TipRanks in the last 3 months, 6 rate APHA a “buy,” while only one says “hold.” Meanwhile, at an average price target of $8.61, the potential twelve month gain lands at 78%. (See Aphria stock analysis on TipRanks)

Takeaway

The key investor takeaway is that Aphria has the cash position to survive and thrive the slow rollout of cannabis sales in Canada. The last quarter’s cash balance above C$400 million and the recent C$80 million financing for the Aphria Diamond facility provide the liquidity for the company to make game changing moves at a time when the industry as a whole lacks financing to expand or engage in accretive acquisitions.

Investors should brace for a guidance cut for FY20 and capitalize on any related stock weakness. Aphria is positioned to take market share as catalysts are unleashed by mid-year 2020.

To find good ideas for cannabis stocks trading at fair value or better, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.