Since the announcement that Constellation Brands fired Canopy Growth (CGC) co-CEO Bruce Linton, the cannabis sector has been under immense pressure, as the face of the industry and the company that was the darling of analysts and pundits came crashing down, resulting in the entire cannabis industry taking a hit it still hasn’t recovered from.

It also didn’t help when the CannTrust (CTST) debacle was reported on in the same news cycle. That is continuing to attract more attention than the issues surrounding Canopy Growth’s leadership challenges.

While the news media predictably focuses on perceived credibility issues in the cannabis industry, I believe that is actually having much less of an impact on investors than what happened with Canopy Growth. After all, it’s not like CannTrust has the flu and by sneezing somehow passes it on to the rest of the sector.

In this article we’ll look at why Canopy Growth had much stronger and lasting of a negative impact on the cannabis industry, and why it’s only going to be temporary in duration; much of the time frame will be determined I believe by the upcoming earnings reports from important competitors like Aurora Cannabis (ACB).

If Aurora and others show meaningful progress and results, the Canopy influence will significantly wane. If not, the impact could linger on because of the conclusion the industry is going through strong growing pains.

The mighty Canopy Growth has fallen

For some time I’ve been publicly sounding the warning signal that Canopy Growth was the wrong horse to bet on in the sector.

The reason for that is Canopy went after recreational pot sales in Canada very aggressively, and that attracted the notice of investors, analysts, and ultimately, Constellation Brands. When Constellation Brands made its big investment in Canopy, the market cheered and rewarded the company with a huge valuation.

This was setting Canopy on a pedestal that was premature, and as the company has started to falter on sales and increasing losses, it triggered the response from Constellation Brands, which now controls the board, and by extension, the company, to fire Linton.

Desjardins analyst John Chu, which is among Canopy’s skeptics, recently noted, “The surprising loss of co-CEO and chairman of the board Bruce Linton is a blow to the company, in our view, and likely creates near-term uncertainty with respect to the company’s leadership and direction.” (To watch Chu’s price targets, click here)

My outlook on Constellation has always been it was looking at taking control of Canopy one way or the other. That’s why it required two board seats and the authority to appoint two independent board members in exchange for the cash infusion.

It also had warrants in place that if exercised, would give the company a 56 percent stake in Canopy. So either way, Constellation was going to control Canopy Growth, and it’s obvious it was waiting for the opportunity to put the people it wanted in key leadership positions. That last disappointing earnings report was the tipping point for that to happen.

The reason it was so devastating on the cannabis industry was because Bruce Linton had become the face of the sector, and Canopy Growth the presumed future of the industry.

So when Constellation Brands took the step of firing Linton, it not only removed the face of the industry, but it also told the market it wasn’t satisfied with the performance of the company.

When the market saw the aura surrounding Canopy Growth ripped away, it started to understand it has not been paying attention to the many risks associated with the company’s business model.

The overall business model

According to Bruce Linton, the company wanted to use Canada as a means of perfecting the many variables associating with operating its cannabis business, and from there scale it out into other markets.

The problem with that is he primarily targeted recreational pot, and fell behind other companies in the much more lucrative medical cannabis segment. It also was a risky strategy because recreational pot comprised of dried flower was a commodity business that was at immediate risk to falling prices.

Another issue is while the company stated it was focusing on the Canadian market primarily, in its actions it started acquiring companies or entering into partnerships in a number of other nations, culminating in its deal with Acreage Holdings in the U.S.

The point is there was confusion in its business model when considering what was communicated, and the actions the company was taking. I believe that came directly from the probability Linton was attempting to do things his way, while Constellation Brands was fighting with him to do it their way. Almost certainly that was where the divorce came from.

The potential future of Canopy Growth

With Canopy Growth losing momentum in the Canadian recreational pot business in the last quarter, and a big deal with Acreage Holdings that may take years to being results, if the proposed acquisition is ever consummated, it looks like to me that Canopy Growth is in legitimate danger of its performance getting much weaker.

With Constellation Brands defending itself from taking a big hit from the losses associated with Canopy, it appears it’s going to primarily focus on cutting losses at the expense of revenue. It will of course never admit or confirm that, but the reality is Linton lost his job because of disgruntled Constellation shareholders that were not happy with how Canopy was dragging down Constellation’s share price.

Now that a number of competitors that were under Canopy are ramping up production capacity, and Canopy apparently lowering spending, how it’s going to maintain the lead it had not too long ago is very questionable.

If Canopy gets less aggressive in regard to production capacity growth, it’s not going to have that much of a lead on the companies it has formerly led by a wide margin.

With a more defensive strategy being deployed to lower costs, the future growth trajectory of Canopy no longer is as compelling as it once had been.

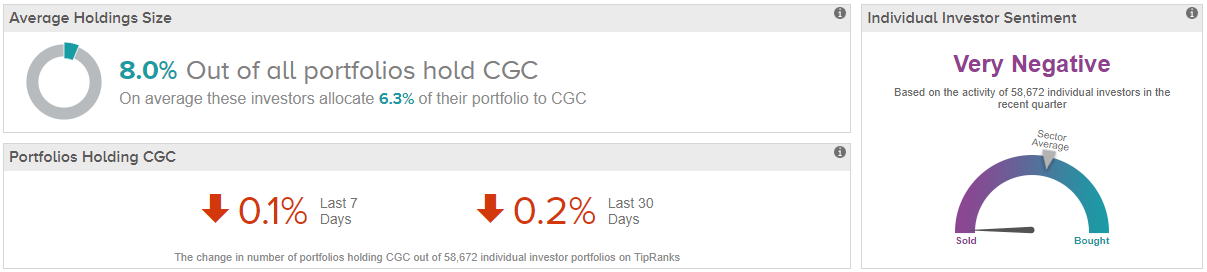

Unsurprisingly, investor sentiment is also very negative, with individual portfolios in the TipRanks database showing a net pullback from CGC.

Conclusion

Canopy Growth was considered to be the future of the cannabis sector, and while I’ve never believed that, the fact that the market did at the time of Linton’s firing after the weak earnings report, has temporarily crushed the cannabis sector.

The good news to me is we can now be rid of that illusion going forward, and if certain companies are market leaders, they’re not going to have the unjustified media support and hype that Canopy Growth enjoyed over the last year or two. That means if a leader disappoints, it’s not going to have the type of effect on the cannabis sector that has come following the fall of the house of Canopy.

While I believe that Canopy Growth is going to disappoint going forward, it’s possible Constellation Brands may be able to lower costs while growing revenue. I see no visible path for that to happen, but there is a slight possibility it may be able to generate sales from derivatives to the level they may offset dried flower recreational sales. Under that scenario, it could at least partially mitigate the expected decline in Canadian recreational sales.

However this plays out, Canopy Growth is effectively Constellation Brands baby now, and there will be no one to blame but itself for its performance in the years ahead. My belief is it’s eventually going to wish it had never taken a position in Canopy at the price it paid.

As for Canopy itself, I think it’s going to be considered a decent company in the future, but won’t ever return to the heights of glory it had in the past, primarily from the annointing it received from the media, which it never had a real chance to live up to.

The impact on the cannabis industry will only be temporary, but Canopy Growth will no longer be perceived as it once had been. To me that’s good for the industry, but not so much for the shareholders that have been true believers.