As the sell-off in the cannabis sector continues, questions on the long-term performance of Aurora Cannabis (ACB) have risen to the point the company is at times presented as a basket case.

While that’s nowhere near to being true, it does point to the need to clarify what the long-term outlook for the company is, and what the major drivers investors need to identify in order to know where the health of the company is at this time.

In this article we’ll look at the three major catalysts that investors need to follow in order to make an informed decision on taking a position in the company, or adding more shares.

The Three Catalysts

The three major things to consider when researching Aurora Cannabis are the potential impact of derivatives on revenue and earnings, production capacity execution, and more GMP-compliant cannabis to sell.

Canada is about to allow cannabis derivatives to be sold in the country. While it’ll be allowable in October 2019, sales are expected to launch until the last couple of weeks of December. That means it won’t have any meaningful impact on Aurora’s numbers until the end of the first calendar quarter of 2020.

Since there have been so many delays in Canada concerning licensing of retail outlets, I’m starting to think it terms of the second calendar quarter being more representative of the potential than the first quarter. In the past I’ve pointed out the first quarter as being indicative of what to expect in the months and years ahead, but I’m starting to be dubious as to how long it’ll take for sales to roll out.

It also remains to be seen how much product Aurora Cannabis will have available for sale in the first calendar quarter. The long-term potential is obvious, but in the near term it may take longer than I originally expected to come to fruition.

Production Capacity

At the end of June 2020, Aurora is expected to have production capacity of well over 600,000 kilograms annually. That will be by far the global leader.

There have been some questions concerning whether or not market demand will reach the level where Aurora will be able to sell its products, but when taking into consideration an increasing amount of that will be used for extraction and to design derivative products, it remains to be seen if it will have too much supply for the market, when considering many of its competitors have been ramping up production capacity as well. It’s too early to tell with the supply/demand equation to know.

Another key factor is a lot of those needing cannabis to sell are looking for consistent partners that can meet their needs for the long haul. Being the market leader in production capacity and supply, Aurora is, in my opinion, going to be the first company looked to to meet supply requirements.

GMP-Compliant Cannabis

Aurora has been finishing up two facilities that were built to be GMP-compliant, which means cannabis grown there will be primarily for the European market.

That’s important to know because the company wasn’t able to grow enough in recent quarters to meet demand in the EU, and that will now change because of the increase in compliant cannabis. This will help boost European sales, which have much more price support than the North American market. In Germany – the most important market in the EU – it has a robust prescription plan in place for medical users to pay for their cannabis.

Aurora has significant exposure to the European market, so will benefit strongly from the increase of compliant cannabis it has available for sale in the region.

Conclusion

The most important takeaway here isn’t only the three major catalysts, but also the timing of them all coming together near the same time.

I see the first calendar quarter of 2020 as being important for the purpose of giving the first snapshot of the impact of derivatives, GMP-compliant pot, and the increasing amount of production capacity on Aurora’s top and bottom lines.

But the really important numbers will come in at the end of June 2020, when all these catalysts come together to form a picture on how the company is advancing with its business model.

I’m still very bullish on Aurora Cannabis, but see the sell-off and continuing delays in Canada concerning retail licensing resulting in them taking longer than I believed to reach important milestones.

By June 2020 most of this should be resolved, and Aurora should be positioned for a powerful and long-term sustainable growth. That could happen as early as the end of the first quarter of calendar 2020, but I’m starting to think June will be more indicative of where the company is at in its growth cycle.

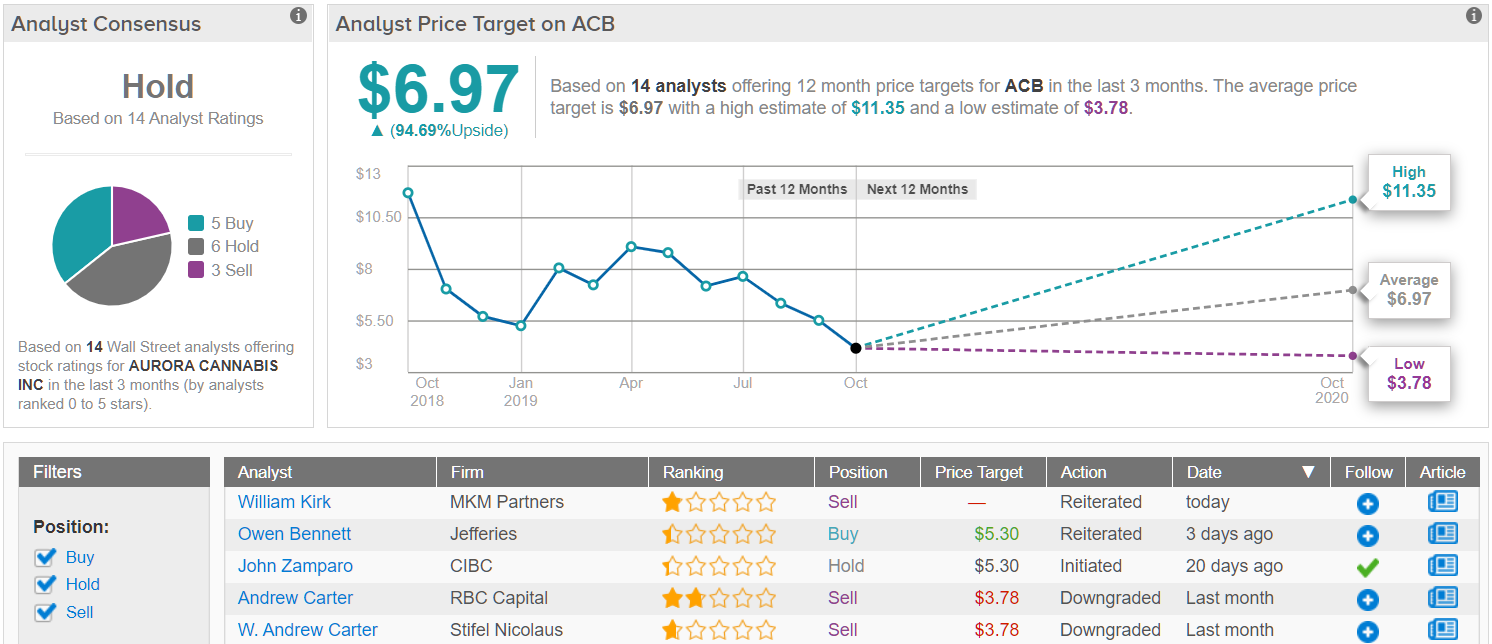

According to TipRanks, the consensus on Wall Street is that Aurora Cannabis stock is a “hold” for investors. But TipRanks might as well have said “buy” — because analysts, on average, think the stock, currently at $3.58, could zoom ahead to $6.97 within a year, delivering 95% profits to new investors. (See Aurora Cannabis stock analysis on TipRanks)