The U.S. CBD sector held so much promise after the government approved the 2018 Farm Bill. Market research firms stared placing total addressable market targets topping $20 billion in a few years, but the FDA has left the market to mostly just lotions and creams leaving the high demand products off major retailer shelves.

At the same time, thousands of different brands have flooded to the space including ones from the large Canadian cannabis LPs. Both Aurora Cannabis and Canopy Growth, amongst others, have launched brands in the U.S. due to CBD being legal in the U.S pushing the brand totals above 2,000.

CBD is the non-psychedelic version of marijuana associated with health and wellness products. Unfortunately for the market segment, the FDA has a mandate to require testing on food products declassified as a Schedule I drug. CBD falls into this category and the majority of the potential sales boost from CBD is tied into ingestible products like foods, dietary supplements and beverages.

The sector is left mostly selling lotions and topical creams where product demand is normally around 15% of the total market demand. For the most part, mass retailers haven’t been willing to take on products under regulatory scrutiny by the FDA. The market once targeted at $20 billion in sales is now forecast by BDS to reach $12.3 billion in 2022 while Jefferies only predicts a market of $3.5 billion as the current pace and regulatory dynamics limits growth.

The key here is that the related CBD stocks are now appropriately beaten down for the worse case scenario. The positive news from the coronavirus outbreak is that medical cannabis was considered essential in a sign that the regulators and governments continue to view cannabis products as essential parts of life leading to speculation the U.S. federal government will approve regulation allowing the expanded sales of CBD by requiring the FDA to remove any restrictions will pushing forward with testing.

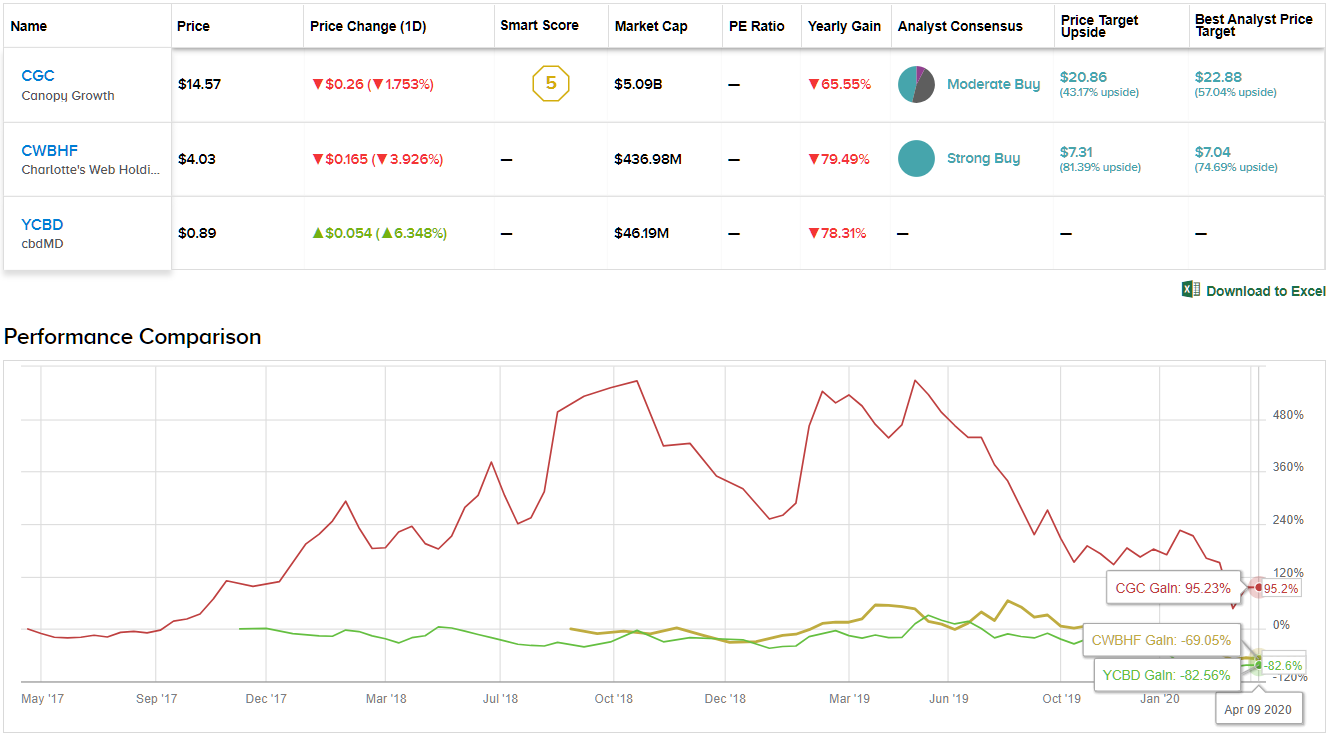

We’ve delved into three stocks set to benefit from ramped-up sales in CBD space. Using TipRanks’ Stock Comparison tool, we lined up the three alongside each other to get the lowdown on what the near-term holds for these CBD players.

Canopy Growth (CGC)

Canopy Growth is the new play in the space. Originally, the large Canadian was wasting money heading into the crowded U.S. cannabis space, but now the space is largely fragmented and likely to lose a ton of smaller players during the economic shutdown.

Some of the estimates of the U.S. CBD market space alone match or even exceed the cannabis space in Canada. Canopy’s first and foremost product has a better opportunity to grab shelf space now and the company could use their balance sheet to purchase some struggling players in the industry on the cheap. Similar to the Abacus Health acquisition by CWH, Canopy Growth could easily snap up some CBD brands in the U.S. on weakness and spend far below $100 million.

At $14.50, the company only has a market cap of $5 billion with FY21 revenue estimates of $500 million. When Canopy Growth was originally forecasting 2020 sales topping $1 billion, the U.S. CBD market appeared more of a distracting move by the company. Now, a sudden removal of FDA restrictions could actually make the CBD product a prime revenue generator of the business.

Canopy Growth was already a buy in the low teens and a big boost in the CBD space will magnify the market opportunity. The large Canadian player has far more capital to thrive via a protracted tough regulatory environment.

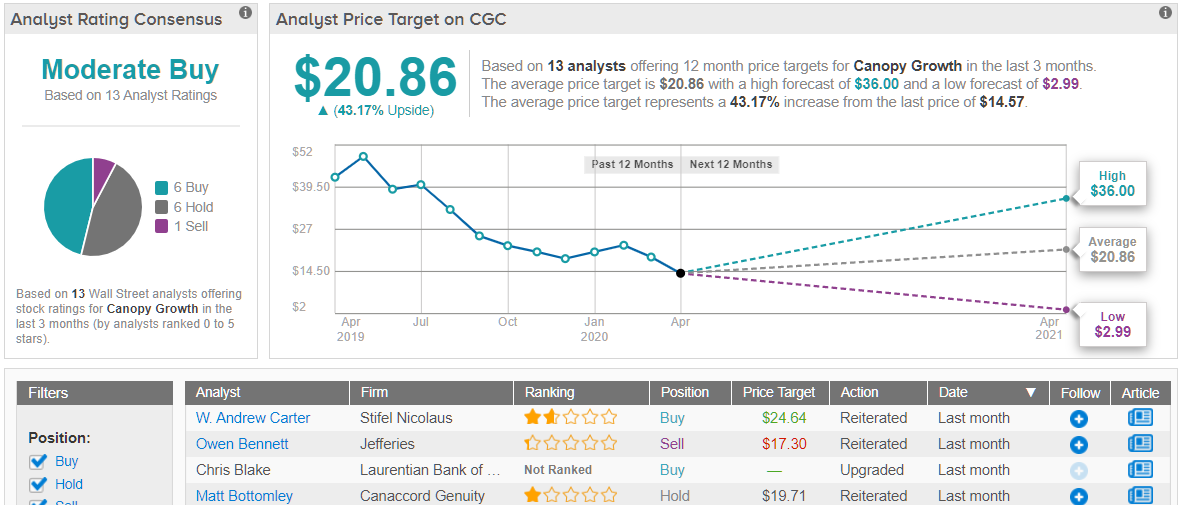

TipRanks points to analyst sentiment split between confidence and caution on Canopy Growth shares. Out of 13 analysts polled in the last 12 months, 6 rates CGC a Buy, 6 say Hold, while only 1 suggests Sell. However, the consensus average price target stands at $20.86, marking a 43% upside potential from current levels. (See Canopy stock analysis on TipRanks)

Charlotte’s Web Holdings (CWBHF)

The ultimate signal for the health in the sector is Charlotte’s Web Holdings. The company is the clear independent leader in the U.S. CBD space and the stock hit a new 52-week low below $3 in March.

The stock now has a market cap below $500 million while the original sales goal for this year was $350 million. Analysts even forecast 2021 sales topping $500 million as recently as mid-2019.

Any signs of health in the CBD sector will first be seen via a boost in the stock price of CWH and the quarterly results. With the acquisition of Abacus Health Products, the company has access to over 15,000 unique retail doors plus some 16,500 health provider offices to expand distribution and consolidate market leadership in the space.

CWH just needs the FDA to clear up the regulatory uncertainty surrounding food products and business will soar. H.R. 5587 would amend the Food, Drug, and Cosmetic Act to remove the requirements placing regulatory restrictions on food products. The new company will only trade at ~1x sales estimates once the FDA relaxes regulations.

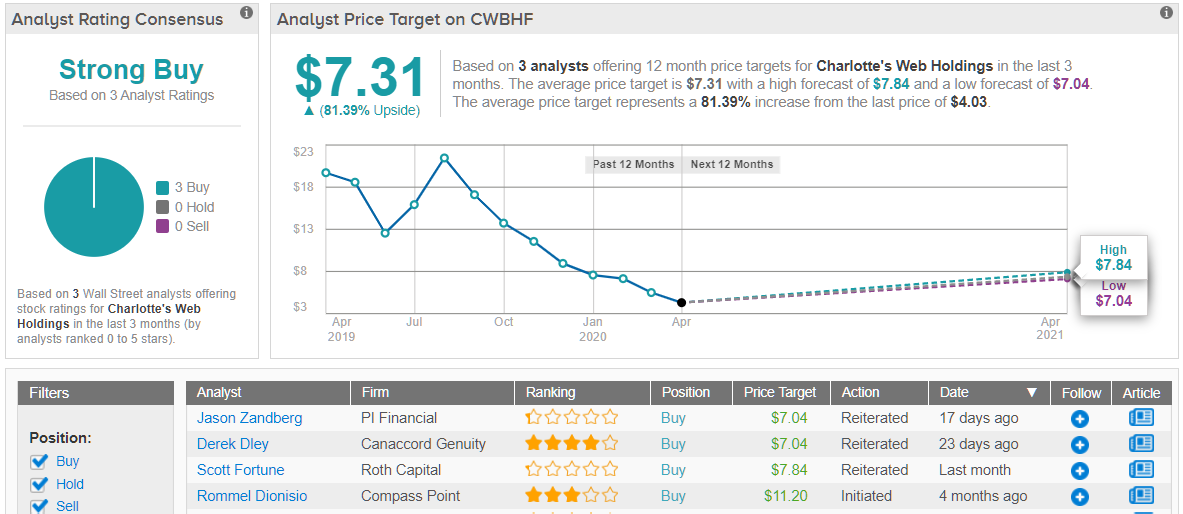

With 3 recent Buy ratings under its belt, CWH gets a Strong Buy from the analyst consensus view. The stock is a bargain at $4 and with an average price target of $7.31, an 81% twelve-month rise could be in the cards. (See CWH stock analysis on TipRanks)

cbdMD (YCBD)

cbdMD continues to trade near all-time lows below $1 following preliminary FQ2 numbers. The company focused on CBD sales saw revenues hit $9.4 million in the quarter, as sales were hit by the FDM mass market where the Covid-19 pandemic impacted sales.

The company operates under the cbdMD and Paw CBD brands with a high reliance on influencers to sell products via their e-commerce site. While cbdMD expanded to over 5,300 retail doors, total tales were still driven predominantly by their e-commerce channel with over 70% of FQ2 sales from this channel.

As with other CBD focused players, the company generates gross margins in the 65% range. Unfortunately, cbdMD has to spend $5 million in the marketing and sales area in order to drive sales leading to a net loss of about $5.1 million in the prior quarter after stripping out non-cash charges.

The company has an improved cash balance of $14.5 million at the end of March. The stock is the speculative play of the group with investors buying this stock in a scenario where the FDA relaxes regulations on CBD food products sooner rather than later.

To find good ideas for cannabis stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.