As Canada heads towards Cannabis 2.0, the stock market will start looking towards companies that provide more value than pure dried cannabis cultivation output. Companies that offer high value services to the industry without the large capital investments required to build massive growing facilities will garner more investor appeal and higher stock valuations.

The cannabis extractor space is just the area to watch going into 2020 as the companies become more valuable with Cannabis 2.0 products requiring more specialized capabilities from integrated extraction service providers. The sector is generally focused on bulk oil extracts now, but the move into beverages, edibles, vapes and concentrates will require more complex capabilities and facilities.

The key here is that while pot has been grown illegally for centuries by various individuals and groups, the market for cannabis extracts is relatively untapped. Companies moving up the value chain should grab higher margins while not having to compete with illegal sources. The extraction of cannabis concentrates is a complex and potentially dangerous process and should only be performed by trained professionals providing a market advantage to the companies with these capabilities.

Any company that can grab market share in this area and establish themselves as a leading provider of high-quality extraction services and product testing will reward shareholders. The future market has the potential to shift towards 75% oil based products according to Cowen Equity Research leaving the companies involved in the extraction and product development process as the potential future market leaders.

We’ve delved into three small companies poised to profit from the demand for third party cannabis extraction services and the development of high-value add products:

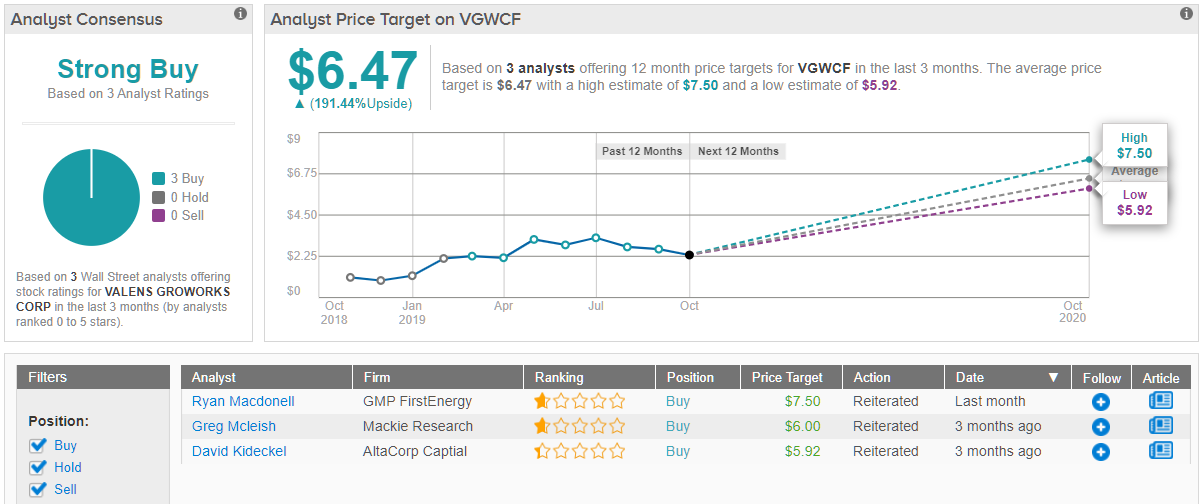

Valens GroWorks (VGWCF)

One of the major players in the cannabis extraction business is Valens GroWorks with contracts with 5 of the top 10 cannabis companies in Canada. The company is building a large extraction facility with a target for 1,000,000 kg of annual throughput while having 240,000 kg in demand from customers for 2020.

The company recently updated guidance for Q3 to revenues of $16 million to $17 million, up from only $8.8 million in the prior quarter. Valens GroWorks projects extracting 26,000 kg of cannabis and hemp biomass in the quarter ending in August with 50% of the extractions taking place in the last month.

The company is in the process of moving annual processing capabilities from 425,000 kg of cannabis and hemp biomass to 1,000,000 kg by early 2020. In the process, the company forecasts reaching $218.1 million in 2021 revenues with over $100 million in EBITDA profits.

Valens GroWorks generated a solid $2.0 million in EBITDA profits in the last quarter and another quarter of huge profits would push the stock higher in an industry where losses are very common now. The cannabis extraction company has the additional catalyst of listing on a major stock exchange in the future. With a fully diluted share count of 140 million shares, the stock is relatively cheap at a market cap of only $325 million.

The stock is an incredible value of below 4x EBITDA targets for just a year out from where the market will start looking at 2021 estimates.

Over the last three months, Valens GroWorks stock has received 3 Buy ratings. As a result, the stock has a ‘Strong Buy’ analyst consensus rating. These analysts believe (on average) that the cannabis stock has big upside potential of over 190% from the current share price. This would take Valens from $2.22 all the way to $6.47. (See Valens stock analysis on TipRanks)

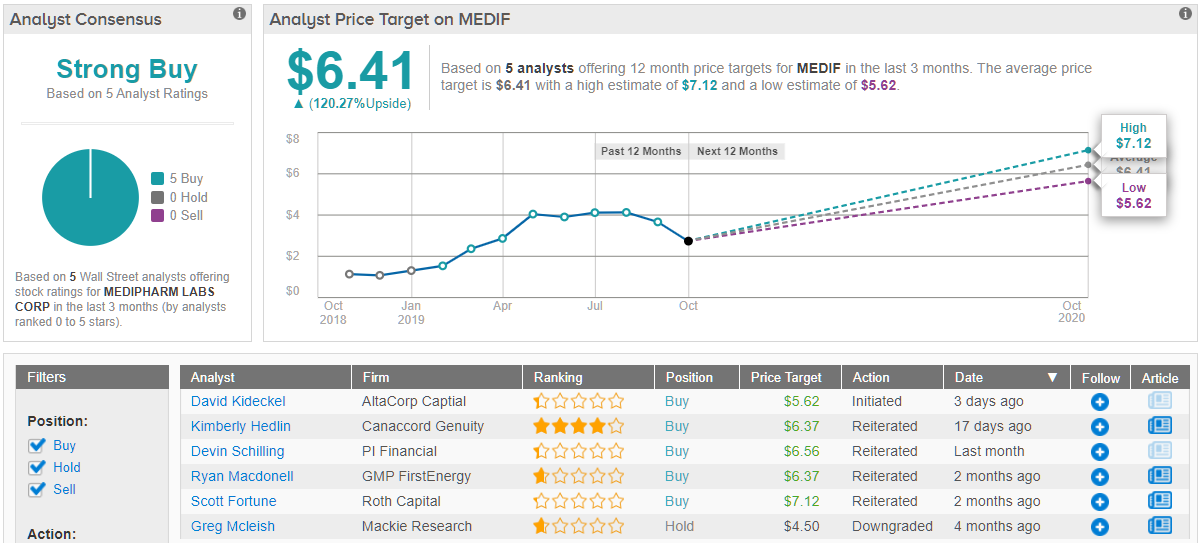

MediPharm Labs (MEDIF)

The largest company in the space is MediPharm Labs with quarterly revenues of C$31.4 million. In the quarter ended June 30, the company generated C$7.7 million of EBITDA for an impressive 24% EBITDA margin.

Similar to the industry, MediPharm Labs is in the process of expanding extraction capabilities. The company recently reached 300,000 kg of extraction capacity with the plans to increase annual capacity to 500,000 kg via the expansion of the facility at the Barrie, Ontario headquarters.

The company already has medical cannabis concentrate supply deals in both Germany and Australia making for a global play without all of the high costs of having massive global operations. In addition, MediPharm Labs has at least four large contracts with the likes of Canopy Growth and Cronos Group.

MediPharm recently closed a $75 million bought deal financing to provide the capital needed for expansion while operations are expected to generate significant EBITDA in the coming year. At $3, the stock has a market valuation of only $385 million.

The extraction-service provider is without question a Wall Street favorite, considering TipRanks analytics indicate MediPharm as a Strong Buy. Out of 5 analysts polled in the last 3 months, all 5 are bullish on the stock. With a return potential of about 120%, the stock’s consensus target price stands at $6.41. (See MediPharm stock analysis on TipRanks)

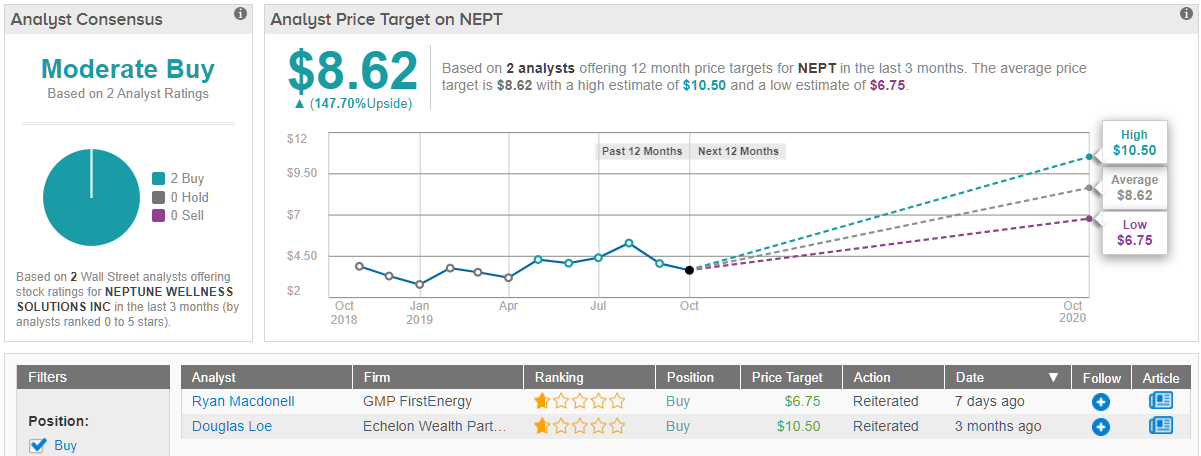

Neptune Wellness Solutions (NEPT)

Neptune Wellness Solutions is the wildcard in the sector after generating a large C$6.5 million loss in the last quarter on only C$4.4 million in revenues. The company has big cannabis extraction plans, but the current results are less than impressive with revenues actually declining from last FQ1 levels.

The company recently bought SugarLeaf Labs and Forest Remedies LLC for $18 million in upfront payments and up to another $132 million in cash and stock over the next three years. The extraction capacity of SugarLeaf is expected to reach 1,500,000 kg of biomass by the end of 2019. In addition, Canada operations expanded in September from 30,000 kg of biomass processing capacity to 200,000 kg annually.

Recent deals with both Tilray and The Green Organic Dutchman should quickly expand revenues. The company forecasts the existing facilities will provide for annual revenues of $450 million at only 50% capacity with EBITDA margins of 40%.

The biggest hiccup with Neptune is the unknown financials and the eventual requirement to pay up to another $132 million for SugarLeaf while the company only has a cash balance of $39 million in July.

Neptune has a listed market value of $340 million, but the highest risk due to the financial position and cash outlays for SugerLeaf while being the only stock in the group generating current losses. Even worse, the CFO is leaving.

What do analysts say about this extraction-services provider? TipRanks analytics show two bullish analysts who rate the stock a Buy, and the average price target among the two stands at $8.62 — a whopping 148% upside. (See NEPT stock analysis on TipRanks)