The U.S. cannabis market enters 2020 with plenty of catalysts for higher sales and better profits for industry participants. One of the primary ways to benefit from immediate growth in the sector is via state level approval of medical or recreational cannabis sales while the Federal government slowly pushes towards eventual Federal approval.

The recent start of recreational cannabis in Illinois and Michigan are prime examples of how U.S. multi-state operators (MSOs) can immediately benefit from having existing cannabis operations in a particular state. The state had an estimated $200 million in medical marijuana sales with research predicting sales surging to between $2 billion and $4 billion with adult-use cannabis legalized starting January 1.

The U.S. currently has 11 states with recreational cannabis approved with over 30 states approving various forms of medical cannabis. The easy path to legislative approval lies within these states with existing medical cannabis programs. A primary target being large states such as Arizona, Florida and New York.

As a prime example, Florida has a medical cannabis program already with 300,000 registered patients and 2,600 prescribing doctors. Activists attempted to get a proposed amendment to make adult-use cannabis legal on the 2020 ballot, but voters supporting recreational cannabis at 65% rate might not get the ability to vote until 2022. The ultimate path to legalization appears clear and companies positioned in the Sunshine state will eventually benefit.

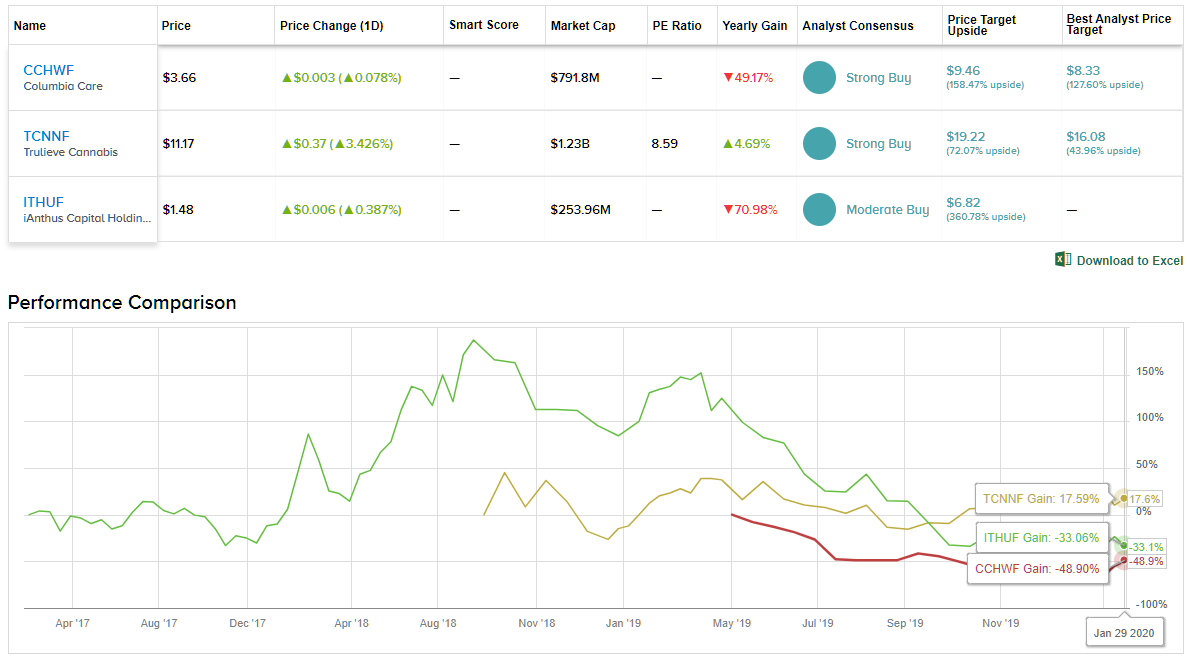

We’ve delved into these three smaller U.S. MSOs poised to benefit from existing medical cannabis states approving expanded adult-use sales. According to TipRanks’ Stock Comparison tool, all three currently have a Strong Buy consensus rating and over 70% upside potential.

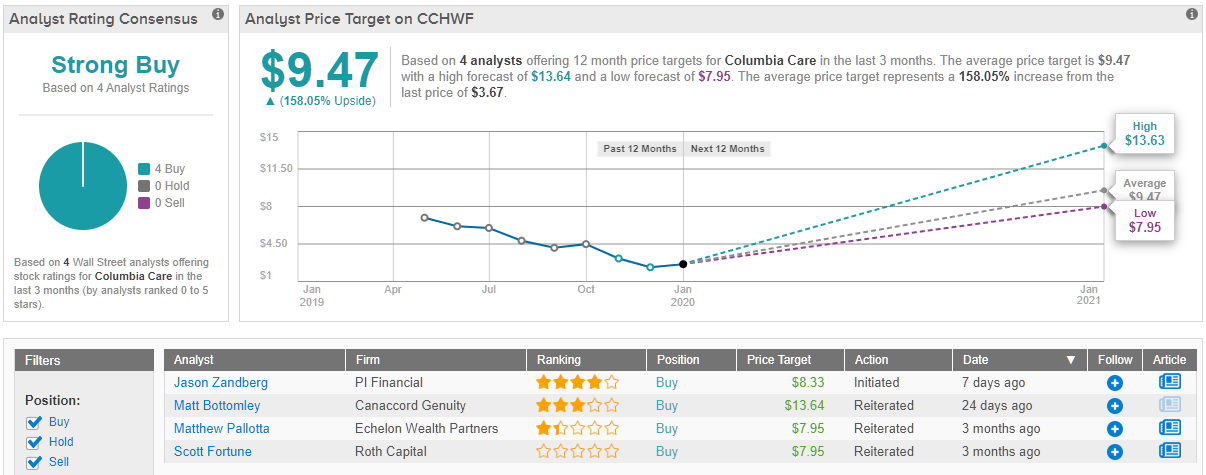

Columbia Care (CCHWF)

Columbia Care is one of the few smaller MSOs set to benefit from both legalization of recreational cannabis in Illinois and the potential addition of Florida in the future. Most MSOs don’t currently operate in both states.

The company recently reported that initial January sales in Illinois grew more than 100% with transactions up an incredible 260%. Adult use sales exceeded medical sales by an incredible ratio of seven to one. The average basket size was down to ~$81 from $110 in the previous medical only program.

The initial sales are promising, but Columbia Care has plenty more to entice investors. The company will open a second dispensary in Illinois soon and recently added four new dispensaries in Florida back in November with the plan to add another 13 locations by the end of 2019. The company expects to have 22 locations open in Florida with 2 manufacturing facilities.

All of these additional sales come on top of Q3 sales of $22.1 million. Columbia Care has operations in 12 jurisdictions with plans to expand into 15.

The stock has a market valuation of $780 million with analyst estimates for 2020 revenue of nearly $250 million. Columbia Care ended Q3 with $85 million in cash and recently completed a $35 million funding leaseback of six properties in California, Illinois and Massachusetts. The company appears well funded for growth in 2020.

The cannabis player is without question a Wall Street favorite, considering TipRanks analytics indicate the stock as a Strong Buy. Out of 4 analysts polled in the last 3 months, all 4 are bullish on Columbia Care stock. With a return potential of nearly 160%, the stock’s consensus target price stands at $9.47. (See Columbia Care’s price targets and analyst ratings on TipRanks)

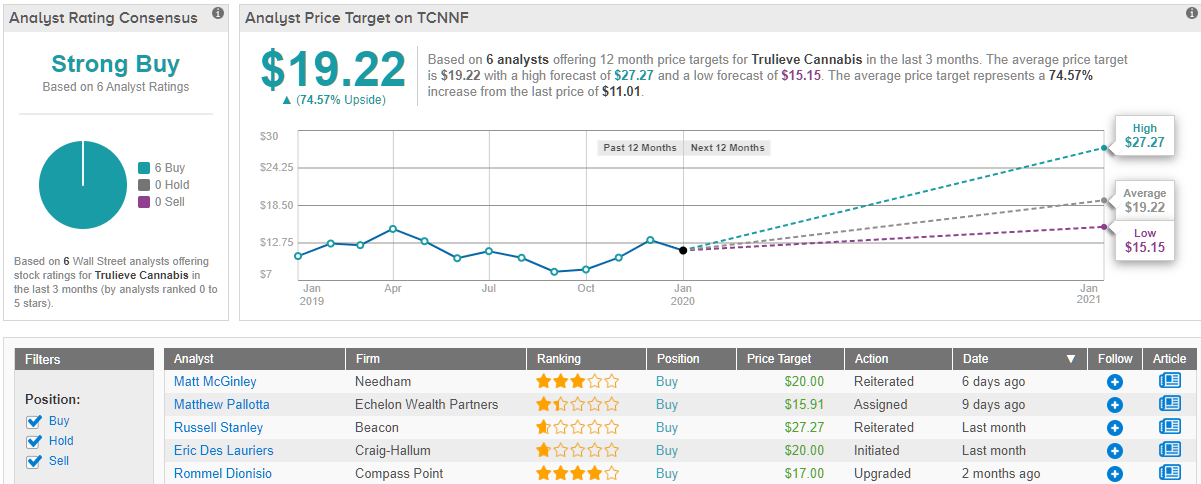

Trulieve Cannabis (TCNNF)

Trulieve Cannabis remains the leading MSO in Florida with roughly 50% market share according to OMMU. The numbers provide a clear path to higher sales when and if the state ever approves recreational cannabis sales. The company recently opened a Fort Walton Beach location to bring the total retail store count in Florida to 43.

The company is one of the best cannabis stories and most controversial. Trulieve reported Q3 revenues of $70.7 million with adjusted EBITDA of $36.9 million. The greater than 50% EBITDA margins almost appear too good to be true and Grizzly Research issued a scathing report on the company.

The report suggested Trulieve creates low-quality weed and has questionable ties to corruption in North Florida. The stock market doesn’t appear to agree as the cannabis stock is only down slightly from the highs around $13 prior to the short attack.

Investors willing to take on this risk get a stock valued at $1.2 billion with 2020 revenue estimates of nearly $400 million. Trulieve continues expanding outside of Florida, but the company only as two dispensaries outside of the key state with the huge potential to participate in recreational cannabis in the future.

Wall Street likes the risk/reward factor at play here, as TipRanks showcases a “strong buy” consensus rooting for Trulieve’s success. In fact, the consensus of analysts following Trulieve is that this stock could rise over 70% in the next 12 months, rising from $11.03 and approaching $19.22 per share. (See Trulieve’s price targets and analyst ratings on TipRanks)

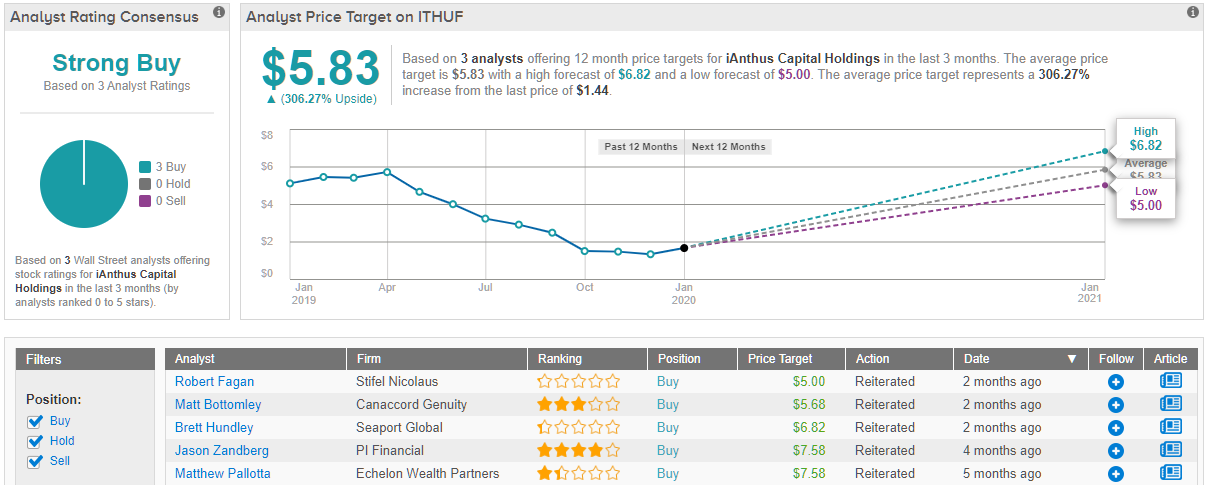

iAnthus Capital (ITHUF)

iAnthus Capital has a network of 30 dispensaries around the U.S. with 12 locations open in Florida. The GrowHealthy brand has a top 10 position in the state with 2.2 million mg sold in the latest weekly report from OMMU ending January 23.

The company has another 10 GrowHealthy dispensaries in the construction or leasing phase. Also, iAnthus is positioned for growth in states like Arizona and New York where recreational cannabis approval could provide a strong sales boost. In addition, the company just got approval for commencing adult-use cultivation and production in Massachusetts making the MSO one of the few set to benefit from the batch of states likely to approve recreational cannabis sales over the next couple of years.

The stock has a market value of $400 million with 2020 revenue estimates of $250 million. The most recent reported FQ2 results generated revenues of $22.9 million with pending acquisitions providing pro-forma revenues of $30.9 million for the quarter.

The company is still generating EBITDA losses and the $100 million funding from Gotham Green Partners hasn’t helped the stock price. The notes issued to GGP have an annual coupon of 13%, payable quarterly, with a conversion price of $1.61.

The market doesn’t like the high financing costs, but the company suggests these investments provide full funding for a capital plan that will get iAnthus Capital to EBITDA positive and operational free cash flow positive this year. The market will reward the stock on reaching those milestones with additional catalysts of recreational cannabis approvals in other operating states in the near future.

Judging from the consensus breakdown, it has been relatively quiet when it comes to analyst activity. Over the last three months, only 3 analysts have reviewed iAnthus. All 3, however, were bullish, making the consensus a Strong Buy. On top of this, the $5.83 average price target puts the upside potential at 306%. (See iAnthus’ price targets and analyst ratings on TipRanks)