The major benefit to U.S. cannabis stocks are the big catalysts ahead for the related companies due to legal changes providing more access to markets. Outside of eventual federal approval, the companies can benefit greatly from the legalization of cannabis sales at the state levels whether for medical or recreational purposes.

In the span of a month, both Michigan and Illinois will start allowing recreational cannabis sales. The Michigan market started this month and is expected to add $600 million in annual revenues while the Illinois market starts January 1 and has the potential of reaching $4 billion in annual sales and building on an existing $250 million medical cannabis market.

For 2020, analysts have forecasted U.S. cannabis sales topping $16 billion while the total global sales may not even reach $20 billion following the weak recreational sales in Canada. The Illinois market alone has the potential of matching the current global market highlighting the massive opportunity for U.S. MSOs.

In addition, Illinois gave a huge advantage to existing medical cannabis companies with the ability to license existing stores plus add an additional store for recreational sales starting January 1. MSOs not in the market already were locked out to this market opportunity with 13 million residents and 117 million tourists annually.

We’ve delved into three U.S. cannabis companies with a strong market position in Illinois that will benefit from the opening up of the adult-use market in under a month. These stocks also fit a double whammy of 1) a bullish outlook from the Street and 2) serious upside potential. That’s vital when it comes to raking in the profits.

We used TipRanks’ Stock Screener tool to find these stocks. We set the following filters: a “strong buy” consensus rating and upside potential of more than 20% from the current share price to the average analyst price target. Then it’s just a question of sitting back and letting the screener work its magic. Let’s take a closer look:

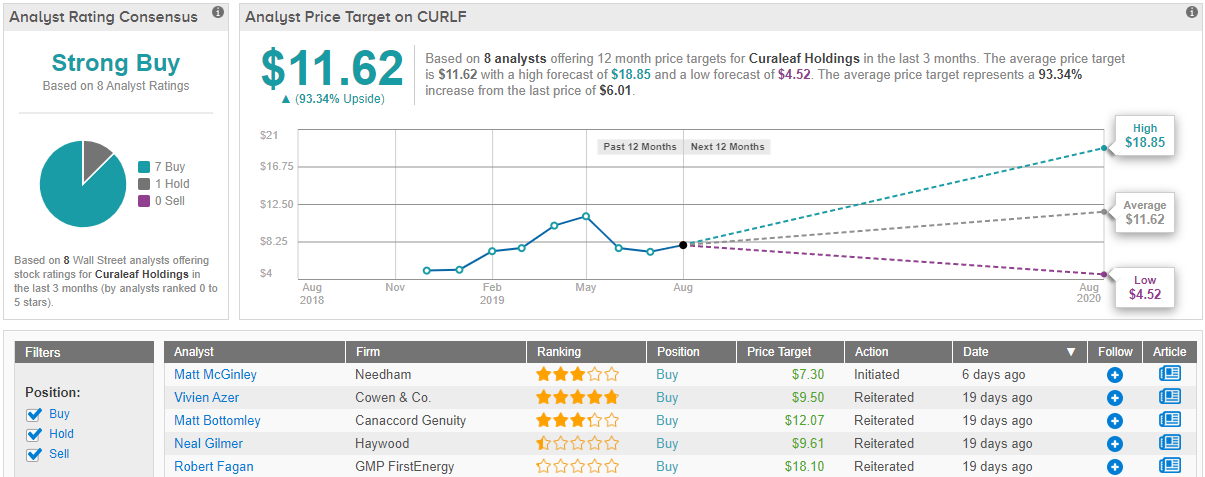

Curaleaf (CURLF)

Curaleaf reported Q3 pro-forma revenues of $129 million. For those paying attention, the U.S. MSO now has far more than double the revenues of the large Canadian cannabis LPs.

The important part to the story with Curaleaf is the planned acquisition of Grassroots with prime operations in Illinois. The deal is expected to close during Q1 shortly after the state opens up for recreational cannabis use. A prime driver of 2020 revenue estimates in a range of $1.0 billion and $1.2 billion and analyst goals for $1.6 billion in revenues by 2021 is the growth opportunity in Illinois.

Curaleaf has 51 existing dispensaries and access to 131 locations with the acquisition of Grassroots. Grassroots has four stores open in the state that were serving the medical cannabis market and the company is allowed to open four more stores including two in the key city of Chicago. A total of 8 stores in the big Illinois market is a huge positive for the stock.

That said, the benefits of the Illinois market and general growth are still highly reliant on the closing of the Grassroots deal providing the stores in Illinois. In addition, the Select brand acquisition to build on market share in the California market is still awaiting final close in January. Until these deals close, the market is very hesitant on the stock.

Curaleaf has a fully diluted market value of $2.8 billion based on 464 million shares outstanding. The deals push the diluted share count to 668 million shares including the 41 million contingent shares for Select. The stock has the potential for a total market value approaching $4.0 billion or only 2.5x 2021 sales estiamtes.

Overall, the U.S. MSO stock remains a Wall Street darling, as TipRanks analytics showcasing Curaleaf as a Strong Buy. With an average price target of $11.62, analysts are predicting massive upside potential of 93% for the stock. In total, Curaleaf stock has received 7 ‘buy’ ratings vs. just 1 ‘hold’ in the last three months. (See Curaleaf’s price targets and analyst ratings on TipRanks)

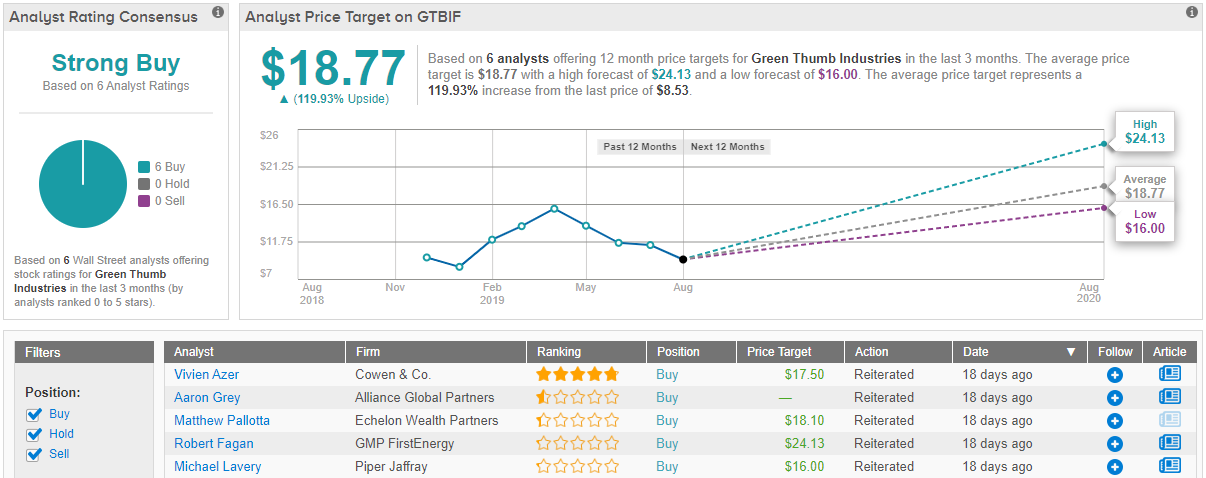

Green Thumb Industries (GTBIF)

Another U.S. cannabis player with a big impact from Illinois is Green Thumb Industries. The MSO located in Illinois has a listed market value of $1.7 billion and originally sold medical cannabis in the state starting back in 2015.

GTI expects to have three adult-use stores open by January 1 with the remaining stores scheduled to open shortly after the market opens next year. The company has five existing medical cannabis stores with the ability to turn those into a total of 10 stores selling recreational cannabis.

As a whole, the company has 34 retail stores open with a goal to reach up to 40 stores this year. GTI has licenses to build 96 dispensaries in the next couple of years.

As mentioned, the stock has a market value of $1.7 billion with revenues estimates set to double to over $475 million next year. The stock trades at a similar multiple of ~2.5x 2021 sales estimates and the stock doesn’t have the same risk of closing pending deals in order to access this key Illinois market.

Wall Street’s analysts have been nothing but bullish on GTI over the past three months. Out of 6 analysts tracked by TipRanks, all 6 are bullish on the stock. With a return potential of about 120%, the stock’s consensus target price stands tall at $18.77. (Discover how the overall stock-price forecast for GTI breaks down here)

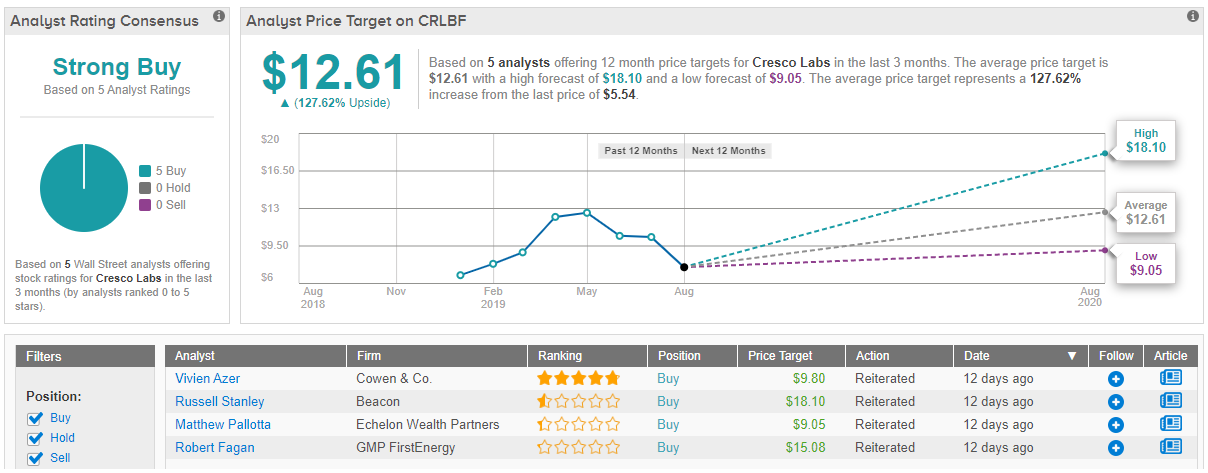

Cresco Labs (CRLBF)

Cresco Labs is the proclaimed leader in the Illinois market with three cultivation licenses in comparison to the two licenses listed by GTI. The company has access to 630,000 square feet of product capacity or 50% more than GTI and 200% above other existing competitors in the key market. Cresco Labs has the ability to supply the other retail dispensaries unlike most competitors.

The company has five medical cannabis dispensary licenses with the access to open five more stores with the approval of recreational use on January 1. In total, Cresco Labs obtains over 65% of current revenues from wholesale sales so the company isn’t as focused on pure store openings as most other companies in the industry.

Similar to Curaleaf, Cresco Labs has pending acquisitions that will impact operations. The company expects to close the Origin House deal soon and recently canceled the VidaCann deal to conserve cash as the market pressures companies needing funding. The stock only has a market cap of $590 million providing a bigger bargain in the sector.

With the existing mergers closing, Cresco Labs will have a market cap of around $1 billion so the company has the biggest impact from the start-up of recreational cannabis sales in Illinois. Despite this huge benefit, the stock trades near the yearly lows.

With only bullish calls issued in the last three months, the word on the Street is that Cresco is a ‘Strong Buy.’ Adding to the good news, its $12.61 average price target indicates the highest upside potential on our list, 127.62% to be exact. (Find out how the Street’s average price target for Cresco Labs breaks down)