We all know that the overall cannabis sector took a big hit in 2019, and it probably won’t start to sustainably recover until after the second calendar quarter of 2020.

While most of the big players with hands on cannabis have suffered enormous downward pressure on their share prices, some pick and shovel cannabis plays, while also participating in the downturn as measured by their share prices, are also positioned to take advantage of the recovery before their counterparts.

In this article we’ll look at Grow Generation, KushCo Holdings, and Innovative Industrial Properties, and what the future holds for them. TipRanks, a company that measures and tracks the performance of analysts, revealed that Wall Street sees each of these names as solid Buys. Here’s what we uncovered.

Grow Generation (GRWG)

Grow Generation primarily offers specialty hydroponic supplies to the cannabis market. At the time of this writing the company had 25 store locations in eight states. In December the company uplisted to the Nasdaq.

In the third quarter it generated revenue of $21.8 million, up 159 percent year-over-year, and up 12 percent sequentially. Operating profits came in at $1.1 million. It has had three quarters in a row of positive EBITDA. The company has guided for 2019 adjusted EPS to be in a range of $0.14-$0.18.

A huge positive for Grow Generation is its hefty 48 percent of organic growth. That points to the markets it competes in having significant demand. It has also benefited from acquisitions and new stores, especially in the Oklahoma market.

The company obviously won’t be able to continue 48 percent organic growth in its stores that have been operational for some time, but it still has a lot of organic growth left in it from new stores.

What’s important for Grow Generation Corp. is it doesn’t matter who wins the battle for market share for those companies touching the cannabis plant; they’ll need what the company supplies no matter who it is.

The major question for Grow Generation over the long term is how it’ll do as competition in its segment heats up. In the near term the company should continue to do very well as market conditions improve and demand for cannabis continues to soar.

The company’s major risk appears to be the availability of capital for its customers. If they struggle to obtain funding, they’ll have less to spend on supplies they need. This could temporarily slow down growth for Grow Generation.

Ladenburg analyst Glenn Mattson recently noted, “As GRWG gains in size it is builidng the infrastruture to support it. GRWG is in the process of implementing an ERP system, which appears to be going well, as gains from efficiencies were listed as a factor in the strong gross margins in the quarter. The company also hired a new COO, Tony Sullivan, who has experience with large retail chains having been Senior VP at Dollar Express (a Family Dollar carve out with 330 stores), as well as 20+ years at Foot Locker serving as Senior VP of store operations in charge of over 2100 stores. This is in addition to bringing in Bob Nardelli, former CEO of Home Depot, to serve as a strategic advisor last quarter. With seasoned leadership our confidence is growing that the company can manage through this rapid growth period.”

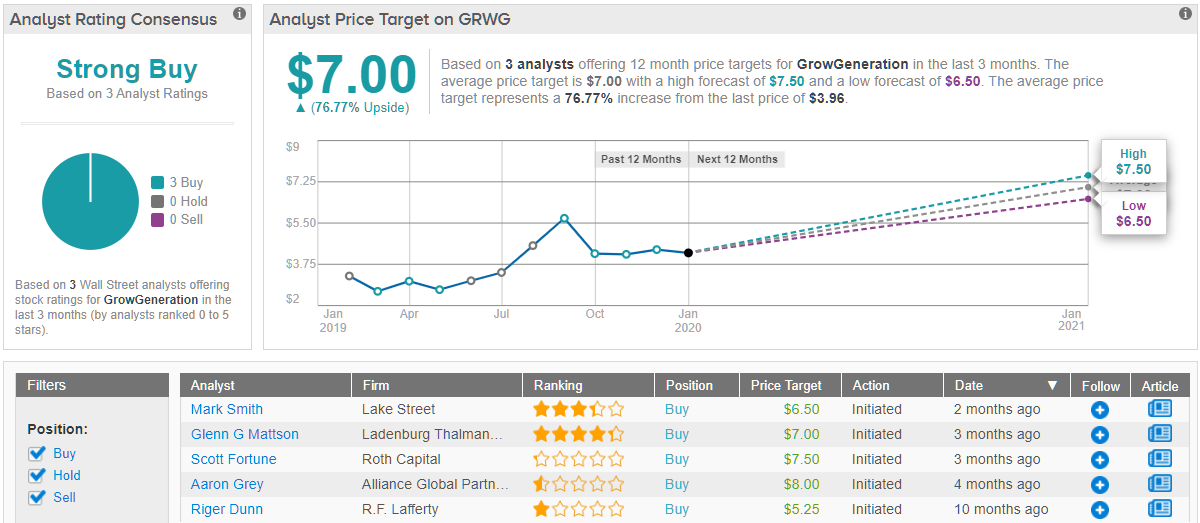

According to Mattson, GRWG is worth over 70% than it’s currently selling for, and should hit $7 within the next 12 months. (To watch Mattson’s track record, click here)

All in all, Wall Street likes the risk/reward factor at play here, as TipRanks showcases a “strong buy” consensus rooting for GRWG’s success. (See Grow Generation stock analysis at TipRanks)

KushCo Holdings (KSHB)

KushCo Holdings is a provider of products and services to the cannabis and CBD industries. In its latest move it entered into distribution agreements with four CBD brands in the U.S. via its partnership with C.A. Fortune.

Its latest quarter it generated revenue of $46.97 million, up 135.3 percent year-over-year, beating estimates by $1.41 million. Non-GAAP EPS in the fourth quarter was -$0.08, beating estimates by $0.04, while GAAP EPS was $11.5 million, or-$0.13, missing by $0.01. The company guided for 2020 revenue to reach over $230 million, possibly climbing to as high as $250 million.

One of the major concerns over KushCo has been its cash flow problems, and even though its margins have improved recently, it will struggle in that regard for some time.

Of the three companies covered in this article, I’m least optimistic with KushCo in the near term. Part of the reason beyond cash flow is it has at times struggled on execution, as in the case of supplying packaging to Canadian companies in the past, where it came up short.

In the long term, it’s the type of company that should do very well in an industry that’s going to grow exponentially over the next several years.

Jefferies analyst Owen Bennett says that KushCo’s “exposure to attractive growing segments in the cannabis space” sees him model “3 year avg. sales growth of 44%, with GM/EBITDA margins growing to 30%/8% respectively from 20%/-11% last quarter. Further accretive M&A also a possibility. In the context of NA peers (basket of 37) its sales profile also impresses, cons. CY21 sales expected at $350mn (Jef $370mn) vs. the peer median avg. of $330mn.”

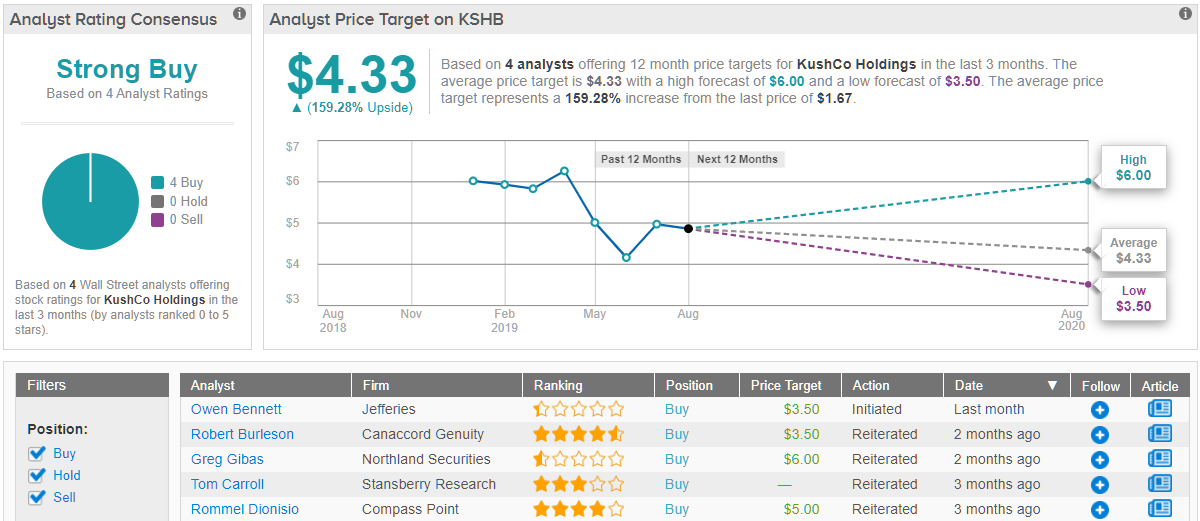

Bennett reiterated a Buy rating on KushCo stock alongside a price target of $3.50, which implies an upside of 110% from current levels. (To watch Bennett’s track record, click here)

Like Bennett, the rest of the Street has high hopes for KushCo. With 4 Buy ratings received in the last three months, the message is clear: the cannabis stock is a “Strong Buy.” At an average price target of $4.33, the potential twelve month gain lands at 159%. (See KushCo price targets and analyst ratings on TipRanks)

Innovative Industrial Properties (IIPR)

Innovative Industrial Properties offers financing in the medical-use segment of the cannabis industry by providing sale and leaseback options, as well as capital.

With pot still illegal in the U.S. at the federal level, banks and other financial institutions have stayed away from financing the sector because of legal issues.

As of its last earnings report it had raised $634 million for its customers, with a reported yield of 13.6 percent.

While it has a great business model at this time, there are several major risks to take into account if considering taking a position in the company.

The first is potential losses of companies if they are put into receivership. One of its clients has already been put into receivership. That could become a problem if that were to escalate if the cannabis market takes longer to recover than anticipated.

Apparently, to combat that the company has decided to focus on stronger clients, the problem there it has had to offer lower rates to win their business; that will put some pressure on its returns.

Finally, there has been a push to deal with financing issues in the U.S. for the cannabis sector by trying to push through the SAFE Banking Act. If it does pass, it would provide hefty competition for Innovative Industrial Properties that would be hard to overcome. That would probably relegate it to providing options to only high risk companies.

The good news on that front is the SAFE Banking Act has run into some roadblocks that make it unlikely to pass any time soon, if ever.

IIPR has a small, but vocal camp of bullish analysts with positive expectations for its stock. Out of the 3 analysts polled by TipRanks, 2 say “buy,” while 1 suggests “hold.” With a return potential of 83%, the stock’s 12-month consensus target price stands at $140.50. (See IIPR stock analysis at TipRanks)

Conclusion

Pick and shovel play winners in the cannabis sector are going to do very well in the years ahead. The cannabis sector is going enjoy significant growth, no matter who the winners will end up being concerning companies that directly touch the plant.

There will continue to be increased competition in the ancillary segment of the cannabis market, but these companies have taken a leadership role in their respective markets, and if they can continue to retain and grow market share, they should do very well over the long term.

For all of the companies talked about in this article, it’s their markets to lose. If they can execute well, they will provide solid returns for investors in the years ahead.

To find good ideas for cannabis stocks trading at fair value or better, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.