As the U.S. economy looks to reopen in multiple states, a lot of American cannabis stocks are still trading near multi-year lows despite limited store closures. The cannabis sector got a major seal of approval with most stores remaining open as states unanimously approved dispensaries as essential stores.

The sector could get a further boost from the need for tax revenues as the whole U.S. tax revenues are down substantially during March and April with the economy shutdown. States from Arizona to Florida to New York could look towards approving recreational cannabis as a way to grab more tax revenues while the Federal government may finally move forward with some real regulations. The government could either approve cannabis or at least provide the companies with access to the banking system and tax relief.

The negative ramifications for the cannabis sector are the tighter credit dynamics, but the large multi-state operators (MSOs) could benefit from weaker players being forced out of business. In addition, a lot of sector leaders are wrapping up or cancelling major deals placing the sector in a more researchable position providing more confidence for investors. Clearly, the market didn’t like the uncertainty in the sector with large deals faltering and taking additional months to close.

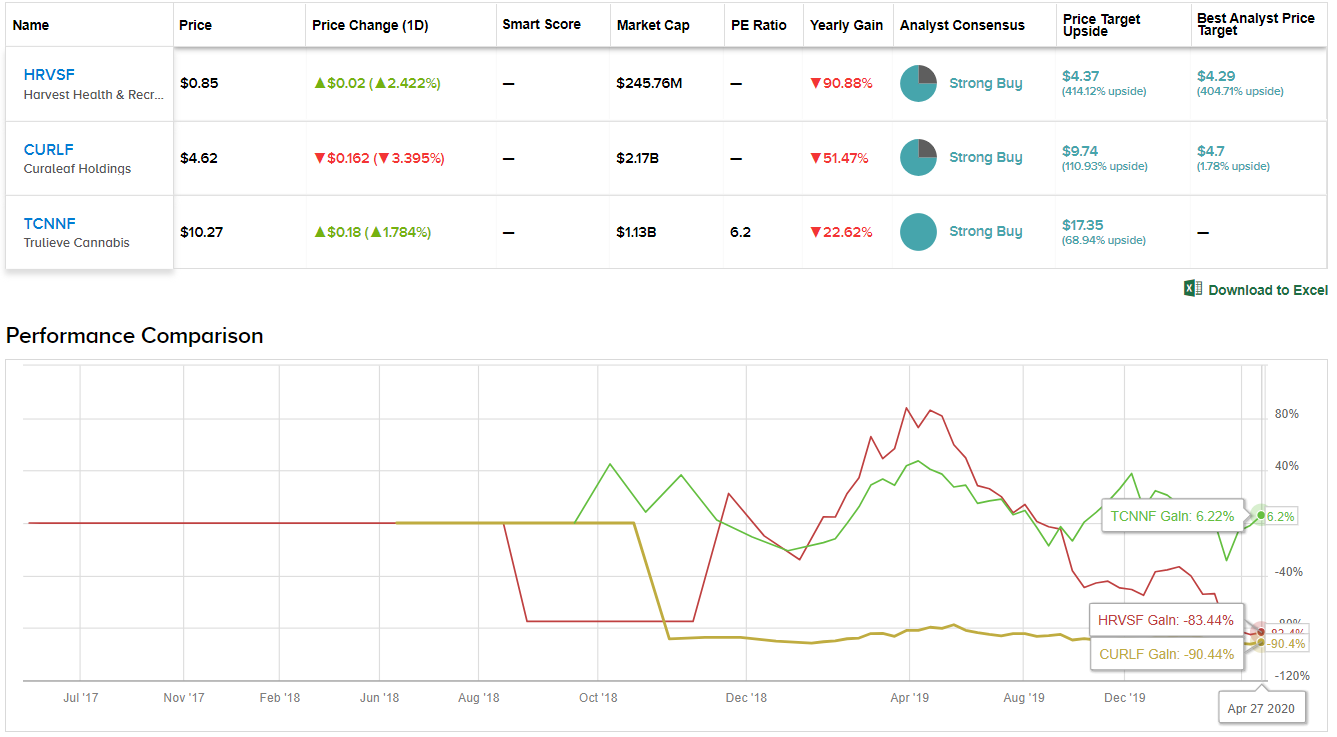

We’ve delved into these three MSOs with positive outlooks for a strong June quarter and catalysts for higher stock prices in 2020. Using TipRanks’ Stock Comparison tool, we lined up the three alongside each other to get the lowdown on what the near-term holds for these MSO players.

Harvest Health & Recreation (HRVSF)

One of the most disappointing MSOs over the last year has been Harvest Health & Recreation. The company ended 2019 with major plans to acquire Falcon and Verano that both collapsed sending the shares to new lows in a weak stock market.

While these deals were supposed to push the MSO into the top tier of cannabis stocks, the company is still on path to top $50 million in quarterly sales during the June quarter. Even better, Harvest Health is positioned in mostly medical marijuana states providing tons of optionality when recreational cannabis gets approved in either Arizona, Florida or Pennsylvania.

A lot of the major deals in the MSO space kept companies like Harvest Health and shareholders alike in limbo. With multiple deals on the table, the valuation was always questioned due to the future share issuance and the unknown complete picture of the new entity.

For Q4, the cannabis company reported sales of only $37.8 million and guided towards Q1 growth at a similar rate as the just reported 14% growth in the prior quarter. Harvest Health should top $43 million in the already ended quarter and be on pace to approach $50 million in the current quarter.

The additional revenues from a full quarter of Arizona Natural Selections will boost Q2 results. Harvest Health ended the quarter with 35 open dispensaries with a license footprint above 100 providing a substantial growth path.

In total, Harvest Health has over 400 million shares outstanding now for a market cap only in the $240 million range while revenues should top $200 million this year before any future benefits of recreational cannabis in key states like Arizona and Florida.

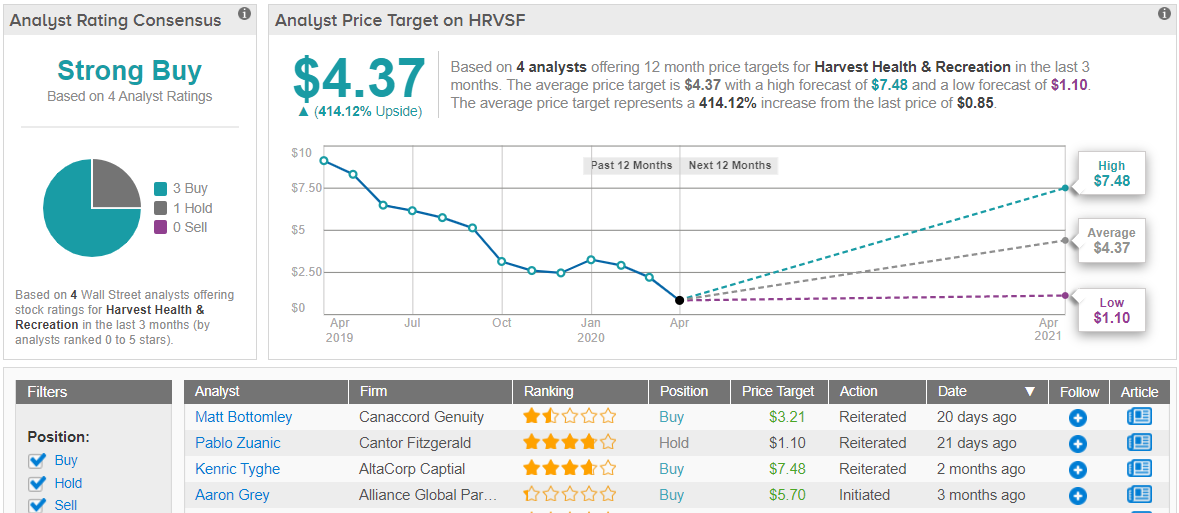

Most of the Street have not given up on the company just yet, as TipRanks analytics showcase Harvest Health as a Strong Buy. Out of 4 analysts tracked in the last 3 months, 3 are bullish on the stock, while 1 remains sidelined. With a potential upside of over 400%, the stock’s consensus target price stands at $4.37. (See Harvest Health stock analysis on TipRanks)

Curaleaf (CURLF)

Curaleaf remains the biggest unknown cannabis company in the world. As the Grassroots deal closes here shortly, the company should have completed a quarter where pro-forma sales should approach $150 million due to recreational sales in Illinois.

While most of the large Canadian cannabis companies have retrenched, Curaleaf continues to expand despite hiccups such as the disappointing Select deal. The resolution of the vape issues should boost wholesales vape revenues going forward and the closure of the Grassroots deal gives the cannabis giants a strong position in the soaring recreational market in Illinois plus expanded access to Pennsylvania.

For Q4, Curaleaf reported official sales of only $82 million with guidance for up to $100 million in the current quarter knowing the Grassroots deal wouldn’t close on time. As mentioned, the March quarter should approach $150 million in pro-forma revenues with an even bigger boost in the June quarter as Curaleaf opens more stores.

After these deals, Curaleaf will have at least 650 million shares outstanding placing the market cap in the $2.6 billion range here. The company had plans for pro-forma sales in the $1 billion range this year and those numbers will depend highly on a rebound in Select brand vape sales and the Grassroots deal closing.

As with these other MSOs, Curaleaf recently closed a deal in just a week for 3 dispensaries in Connecticut. The market will find the certainty of these tuck in deals more appealing going forward.

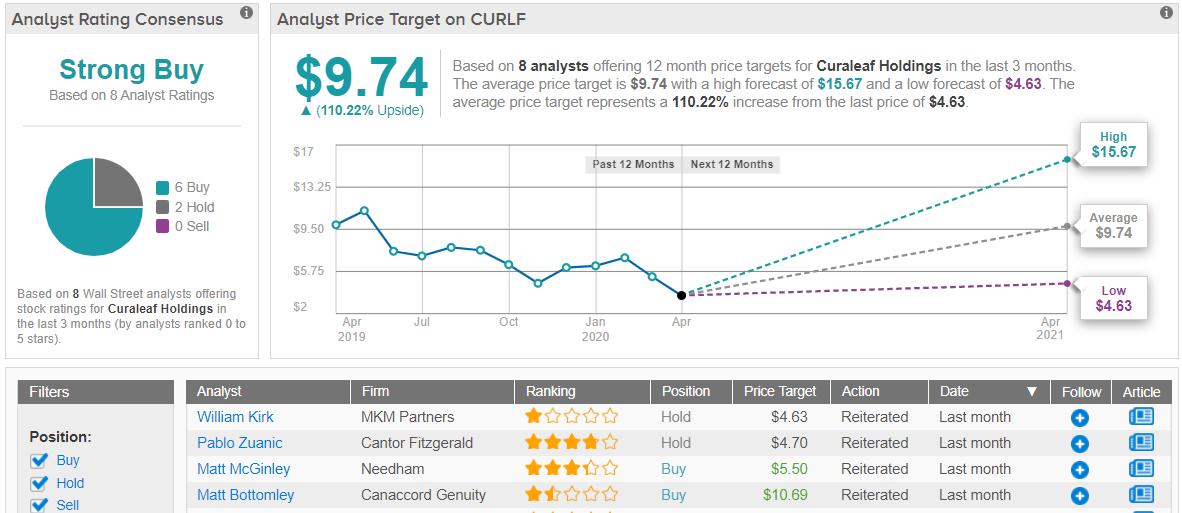

Overall, Wall Street loves Curaleaf stock, considering most voices are betting on this cannabis producer. TipRanks analytics exhibit Curaleaf as a Strong Buy based on 6 Buy ratings and 3 Holds. The 12-month average price target stands at $9.74, marking a 110% upside from where the stock is currently trading. (See Curaleaf stock analysis on TipRanks)

Trulieve (TCNNF)

Another underappreciated cannabis play is Trulieve Cannabis. The stock has bounced off the lows back above $9, but Trulieve traded above $13 back in December and the company reaffirmed strong numbers only a couple of weeks ago.

The MSO has incredible expectations for 2020 adjusted EBITDA of $150 million. While the major Canadian companies are struggling to even reach EBITDA positive levels, Trulieve reported a 22% sequential boost in quarterly EBITDA to $45 million in the December quarter.

The company is mainly just a medical cannabis provider in Florida, so the $400 million revenues estimates for this year is a sparse reflection of the ultimate revenue potential. Considering Trulieve has already confirmed 2020 numbers into April, the stock is de-risked having likely survived the worst of the COVID-19 crisis while benefitting from medical cannabis being labeled an essential product. With a market cap of only $1 billion, the stock is truly underappreciated.

It’s worth pointing out that Wall Street analysts are unanimous in their endorsement of the shares. Trulieve has been endorsed with “buy” ratings by all five of the analysts who have voiced an opinion on the stock over the three months. Meanwhile, the consensus estimate of analysts polled is that Trulieve shares should rise a 68% (68.61% to be precise) to hit $17.35 within a year.

To find good ideas for cannabis stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.