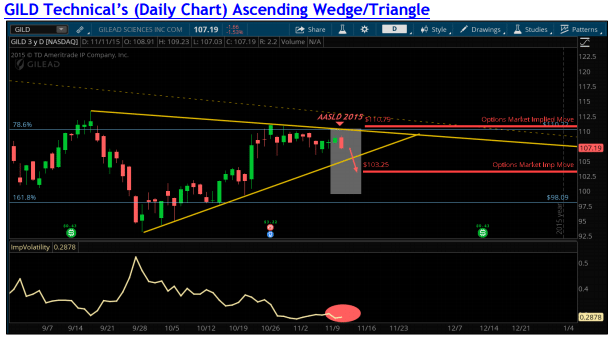

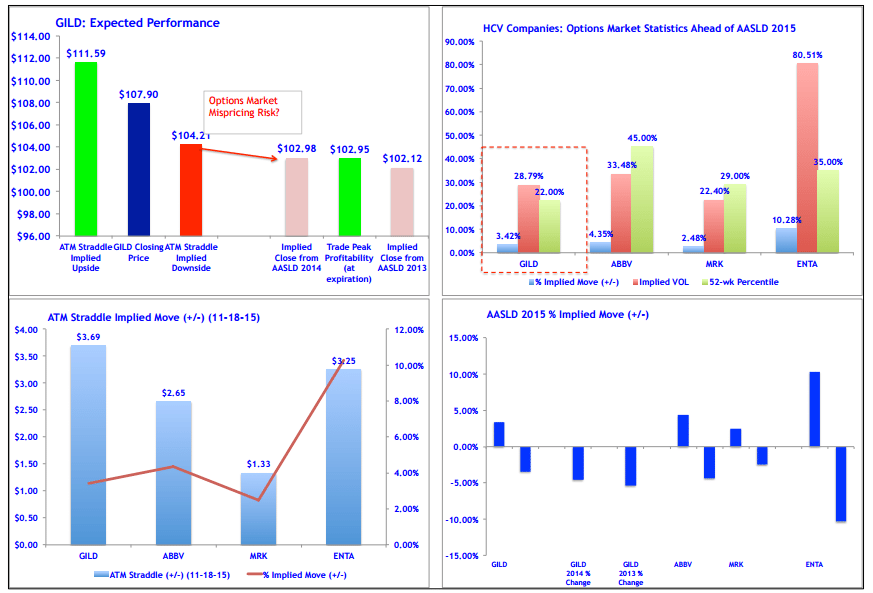

The options market appears to be underestimating the risk to Gilead Sciences, Inc. (NASDAQ:GILD)’s share price ahead of an event that could intensify the bear’s thesis concerning GILD’s sustainability problems due to competitive threats from MRK and ABBV ahead of the 66th Annual Meeting of the American Association for the Study of Liver Diseases (AASLD) Nov 13th-17th. Whether or not they actually represent a threat to GILD’s HCV sustainability is irrelevant here, what the market perceives and how it reacts is all that matters. Implied VOL is curiously low at 28.79% ranking only in the 22nd percentile over the past 52-weeks, and the ATM Straddle is pricing in a +/- 3.42% move by next Friday’s close.

ABBV & ENTA will present interim SVR12 data from their next-gen combination regimen of ABT-493 (NS3/4 protease inhibitor) and ABT-530 (NS5A inhibitor) from two Phase II studies, SURVEYOR- 1(in GT1) and SURVEYOR-2 (in GT2 and GT3). And MRK will be presenting key data from their once-daily all-oral pan-genotypic regimen containing grazoprevir (NS3/4A protease inhibitor)/MK-3682 (NS5B polymerase inhibitor)/MK-8408 (NS5A inhibitor) from their C-CREST-1&2 trials in GT1-3 HCV patients after only eight weeks of treatment in a late-breaking poster session on Monday, November 16, which is a shorter treatment duration compared to GILD’s sofosbuvir+velpatasvir (12 weeks). In our view, MRK represents a troublesome threat to ABBV’s HCV franchise, and only a moderate threat to GILD. As a result, we believe that MRK and JNJ will erode ABBV’s market share to less than 5% by 2018/2019.

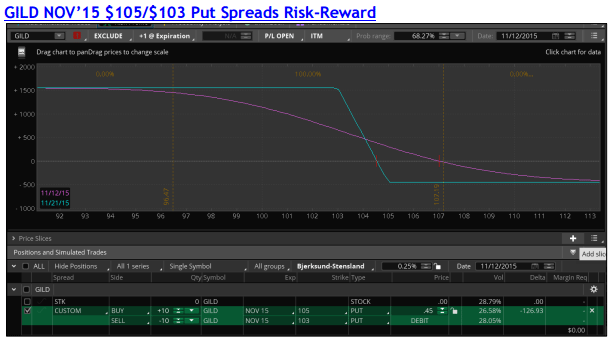

While it has been clear that we are “perma-bulls” on GILD since 2014, we remain so ahead of potential M&A. However, the AASLD conference represents an isolated window of time that we can capture both a swoon in confidence and seasonal/event weakness through a risk-defined trade structure by buying the Nov15 $105/$103 Put Spreads for $0.45-$0.50 net debit that pays out +$1.55 profit if GILD closes below $103 by next Friday’s. This represents a risk-reward of ~3:1 (see trade setup and charts in the following pages).

Moreover, GILD remains an unloved stock; largely range bound the past twelve-months with the market seemingly selling shares off as a source of funds for just about any reason, it’s lack of leadership since the lows on September 29th, 2015 also supports a bearish trade bias going into

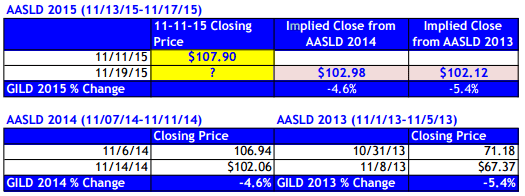

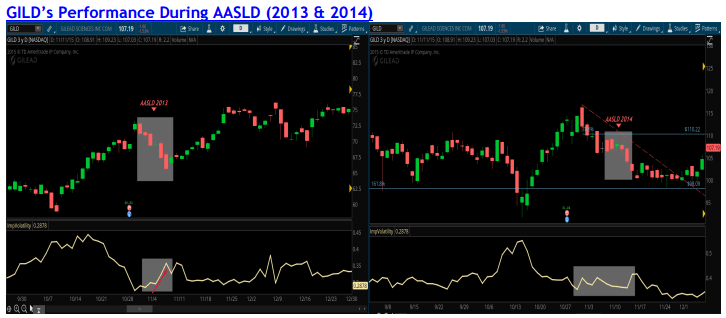

AASLD. We analyzed GILD’s share performance during the AASLD conference since the “post-Sovaldi” era from 2013 and 2014. On both occasions GILD’s share price declined -5.4% and -4.6% respectively, with the options market pricing in only a +/- 3.42% move next week we believe the risks are skewed to the downside and argue that premium is cheap here.

We have been trading options on GILD ahead of events over the past three years, almost exclusively selling premium ahead of events and seldom have we found such cheap premium to purchase put options ahead of an event like AASLD. We analyzed GILD’s share performance during the AASLD conference in the “post-Sovaldi” era from 2013 and 2014. On both occasions GILD’s share price declined -5.4% and -4.6% respectively, with the options market pricing in only a +/- 3.42% move we believe the risks are to downside and argue that premium is cheap here.

Don’t be late to the party – Click Here to see what 4500 Wall Street Analysts say about your stocks.