By Robert Rapier

One question that I have been asked on a regular basis — since almost the start of the decline in oil prices in 2014 — is whether it is time for investors to jump back into upstream (i.e., oil and gas production) MLPs. Today I want to emphasize the risks of these upstream MLPs as evidenced by some of their 2015 financial metrics.

Given the high risk, we don’t normally recommend the upstream sector for most MLP investors. On a historical note, when I started writing this newsletter both MLP Profits andThe Energy Strategist recommended several upstream partnerships, including by far the largest of these, Linn Energy (NYSE: LINE). We kept Linn in the portfolios for a while, and investors who had held since the original recommendation more than doubled their money.

But we became increasingly concerned over a weakening cash flow position and an SEC investigation into its accounting, so on July 2, 2013 we issued a sell recommendation for Linn Energy. On that day Linn Energy units closed at $27.05. Today you could buy a unit of Linn for 35 cents. This should emphasize to investors the significant risks in the upstream MLP space.

But since these producers are an ever-popular topic of inquiry with investors, today I want to list and compare them. For this exercise, I used a proprietary Excel-based screen that utilizes the S&P Global Market Intelligence database. I screened for publicly traded partnerships engaged primarily in upstream operations that reported at least some oil and gas reserves at the end of 2015. Most of these are engaged in oil and gas production, but two of them own mineral rights and rely on royalty payments for distributions. In order of descending enterprise value (EV), they are:

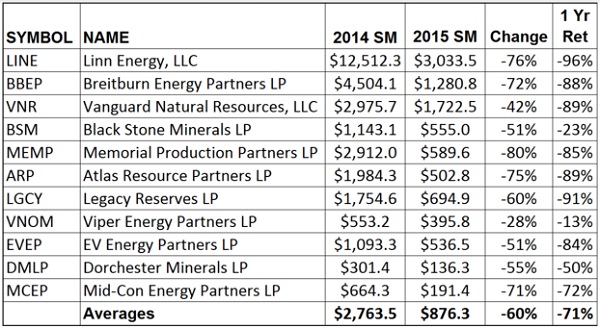

- EV – Enterprise Value in millions of dollars as of March 29, 2016

- EBITDA – 2015 earnings in millions of dollars before interest, tax, depreciation and amortization

- FCF – Levered free cash flow in millions of dollars for the trailing 12 months

- Res – Total proved reserves in million barrels of oil equivalents (BOE) at year-end 2015

There are two significant items to note in this table. First is that a Debt/EBITDA level above about 3 is high. The higher it gets the more difficulty a company will have in paying off its debt. Companies like Linn Energy that have a Debt/EBITDA ratio above 6 will find increasingly limited options in managing their debt, and bankruptcy will loom as a realistic possibility. Don’t let Linn’s $9 billion EV mislead you into thinking otherwise.

In fact, the formula for calculating EV is to take the market capitalization plus debt, minority interest and preferred shares, minus total cash and cash equivalents. Much of the difference between a company’s enterprise value and its market capitalization is typically accounted for by its debt. Inclusion of debt provides a more accurate estimate of the cost of acquiring the company. In Linn’s case, its $9 billion of debt certainly matters a lot more than its $142 market capitalization in evaluating the partnership’s prospects.

The second thing to note from the table is that the two MLPs based on mineral rights —Viper Energy Partners (NASDAQ: VNOM) and Blackstone Minerals (NYSE: BSM) — have very little relative debt. That is primarily because they don’t have the same operating expenses as the conventional oil and gas producers. As a result, they have held up better over the past year than the others. Here is the list again, highlighting some other important performance measures:

- SM – Standardized Measure, the present value of the future cash flows from proved reserves as of year-end

- Change = Year-over-year change in the standardized measure

- 1 Yr Ret = Total unitholder returns for the past 12 months (except for Black Stone, which had its IPO in May 2015)

The first thing to note is the enormous year-over-year deflation in the estimates of future cash flows of these companies. To review, each year the Securities and Exchange Commission (SEC) requires energy producers to estimate the present value of the future cash flows from proved oil, natural gas liquids (NGLs) and natural gas reserves, net of development costs, income taxes and exploration costs, discounted at 10% annually. This calculation is called the standardized measure (SM), and is based on the average prices received over the past 12 months for oil, natural gas and natural gas liquids.

In total, between year-end 2014 and year-end 2015 these companies cumulatively reduced their estimated future cash flows by nearly $21 billion. Linn Energy took the biggest overall hit with a reduction of $9.5 billion. These reductions came about not only because the value of the reserves has dropped with oil prices, but also as some reserves were written off as uneconomical to produce at prevailing prices. Linn Energy, for example, had to reduce its estimate of proved reserves by nearly 40% from the prior year as a result of lower commodity prices.

The second item to note on this table is that VNOM and BSM — again the only two MLPs on the list based on mineral rights — were the only ones not to lose at least 50% of their value over the past 12 months. This suggests that if you want some exposure to the upstream MLP space, this may be a less riskier alternative to the exploration and production MLPs.

Nevertheless, we continue to recommend that investors avoid this space. The tables above highlight the high level of risk. Yes, when oil and gas prices ultimately rebound some of the names on the list will do quite well. But some others will likely be out of business.

And when MLPs go out of business their limited partners face losses beyond the worthless equity. That’s because the debt written off in a partnership bankruptcy is treated as taxable income accrued by the partners, even though these phantom gains don’t represent actual cash flow.