By New Deal Democrat

Several months ago, I made a qualified forecast for continued growth in the second half of 2016. On Friday, the BEA finally reported corporate profits for the 4th quarter of last year. While usually proprietors’ income (reported in the initial GDP release) tracks corporate profits well, sometimes they do lag, and this was one of those times, as profits declined significantly. Beyond that, we now have two to three months of data on the remaining long leading indicators, so this is an important time to update my outlook.

And the news isn’t good.

Let me start with my usual framework. Geoffrey Moore, who for decades published the Index of Leading Indicators, and founded the Economic Cycle Research Institute (ECRI) in 1993, wrote Leading Economic Indicators: New Approaches and Forecasting Records describing and explaining what he called “long leading indicators,” that is, economic metrics that reliably turn a year or more before the onset of a recession. He identified 4:

– housing permits and starts

– corporate bond yields

– real money supply

– corporate profits

A variation of the above is Paul Kasriel’s “foolproof recession indicator,”which combines real money supply with the yield curve, i.e., the difference in the interest rate between short and long-term treasury bonds. This turns negative a year or more before the next recession about half of the time.

Another long leading indicator has been described by UCLA Prof. Edward E. Leamer who has written that “Housing IS the Business Cycle.” In that article, he identified real residential investments as a share of GDP as an indicator that typically turns at least 5 quarters before the onset of a recession.

Additionally, Doug Short has identified real retail sales per capita as another important metric. This metric tops out at least a year before the onset of a recession about half of the time.

Finally, last year I noted that, although it has a limited history, the Labor Market Conditions Index appears to have value as a long leading indicator. So I am adding that to my list.

That gives us a total of 8 long leading indicators. All of these economic series have a long-term history of turning a year or more before a recession. Let’s look at them:

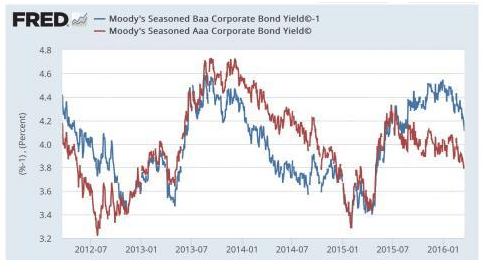

Corporate Bond Yields

Yields for AAA bonds last made a low in 2012. BAA bonds tied that low in early 2015:

As it has been over a year since that low, these are now a negative.

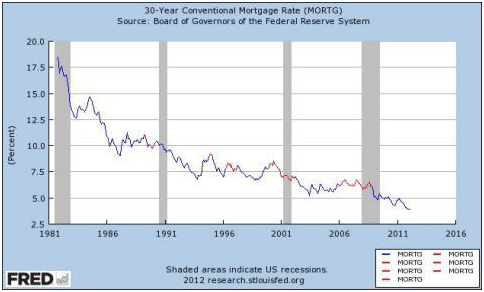

As an aside, I have also frequently noted that when mortgage rates have failed to make a new low for 3 years, the positive effects of the last round of refinancing have dissipated. Since 1982, this has been a necessary predicate for a recession. Mortgage rates last made a new low in November 2012:

These are also now a negative signal.

The (relatively) good news is that bond yields typically rise by 2% or more – and stay there – before a recession begins. Bond yields have done no such thing in the last year. In fact, most of them are close to their lows.

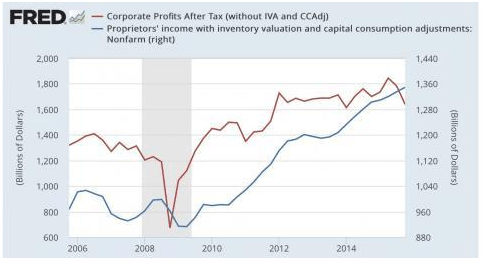

Corporate Profits

As reported by the BEA on Friday, corporate profits declined again in Q4 (red in the graph below), thus failing to confirm the preliminary signal of proprietors’ income (blue):

Corporate profits are a more reliable long leading indicator than proprietors’ income, so this too is also now a negative.

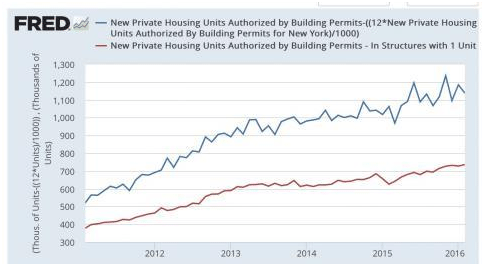

Housing

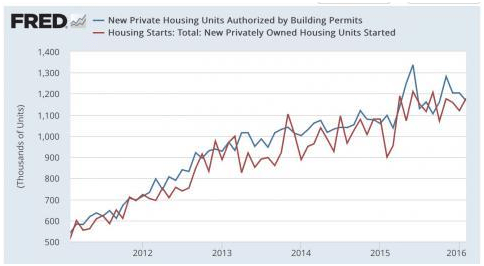

The most reliable housing indicator is permits, as they are less volatile and tend to slightly lead housing starts. These last made a new high this past June:

Since the expiration of an NYC program in June distorted the seasonal adjustments, I have worked around this by making use of permits ex-NY, and single-family permits:

Permits excluding NY last made a high in November. Single-family permits last made a high in November and December, respectively, although single-family permits are only 1000 off that high as of February.

As I wrote last week, it appears that housing has either just passed or is near its peak. I am scoring this a negative – but just barely.

As of the 4th quarter, real residential spending as a percent of GDP had made a new record:

This will not be updated for another month. For now, this is still a positive. But if spending tracks permits, Q1 will be slightly below Q4, and if Q1 GDP is positive, that will tip this indicator as well to negative.

Real Money Supply

No recession has ever started without real M1 turning negative or real M2 being more than +2.5% YoY. Here’s what they look like now:

Both are less positive than before in this expansion. But if they are fading somewhat, they are both still positive.

The Yield Curve

At least in times of inflation, an inverted yield curve, where short rates are higher than long rates, has been perhaps the best of all indicators of a recession a year or so later. Here’s what it looks like now:

This has gone from being strongly positive to just normally positive. But positive nevertheless.

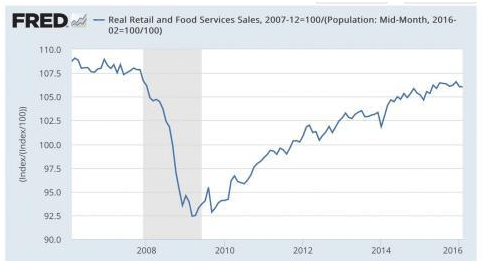

Real Retail Sales Per Capita

The big downward revision of January’s initially strong numbers really put a dent in this indicator:

This is now a negative, but like housing, just barely so.

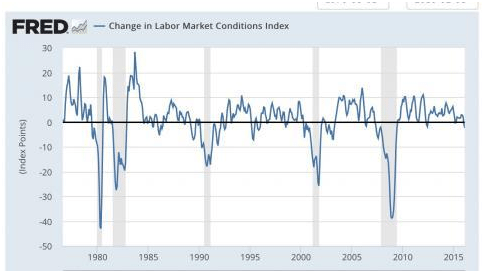

The Labor Market Conditions Index

This Index only dates from the 1970s, so it is not backed up by as much history as the other indicators. But since then, it has been a reliable long leading indicator. With just one exception (1981’s double dip), the index always failed to make a new high for at least 12 months before the next recession, sometimes much longer than that. Further, the index has always dropped below 0 and stayed negative for 6 months or somewhat more before the onset of the next recession.

Here is the entire history of the series through last month:

It decelerated markedly last year, and has been negative two months in a row. For now, this too is a negative.

Summary

Of the 8 long leading indicators, right now only 2 – the yield curve, and real money supply – are positive.

Two more – interest rates and corporate profits – are firmly negative.

One – real residential investment – is positive as of its last report, for Q4 of last year, but looks likely to turn at least slightly negative when Q1 GDP is reported next month.

The remaining 3 – housing permits, real retail sales per capita, and the labor market conditions index – have just turned negative, but only slightly so.

I am reluctant to turn outright negative with real money supply – which typically leads so much that it has returned to being positive even before a recession begins! – remains a firm positive. Another reason is that while bond yields have failed to make new lows, they haven’t spiked either. At the same time, 6 of the 7 remaining long leading indicators are now negative – even if just slightly – or are likely to be so when Q1 GDP is reported next month.

So here is my conclusion. I am not quite ready yet to go on “Recession Watch” for 2017. The data is simply too close to call, and I don’t want to whipsaw back and forth. But the outlook has dimmed sufficiently that we might be in recession as early as Q4 of this year.

I want to see at least one month’s more data on housing, retail sales, and the labor market conditions index, to see if they remain negative. I want to see if real money supply continues to decelerate. On the other hand, I want to see if interest rates react to weakness by making new lows. If these go on to new highs/lows, I will return to a positive outlook. In fact, with the big decline in interest rates recently, I think that is the more likely scenario. But if housing, retail sales and the labor conditions index remain negative or deteriorate further, I will go on Recession Watch for 2017 as early as next month.