Those that follow my biotech recommendations know that I look for undervalued small cap stocks with significant upside. Some may be momentum plays, meaning that the stock is ripe to move upwards based on recent data or upcoming catalysts which are likely to be positive. Generally, these stocks have very little if any analyst coverage and are ignored until positive developments emerge enabling significant gains to be made quickly if one does the proper research. For example, I wrote an article 2 weeks ago detailing why microcap Actinium Pharmaceuticals was a good buy ahead of the ASCO conference. The stock quickly gained more than 80% in 4 days. In fact, the data released at ASCO was largely a reiteration of what had already been disclosed, but simply overlooked. Other recommendations are more long term plays where a company has a solid product that has a high chance of success. For example, I wrote an article suggesting investors purchase Ovascience in late 2013 before any analysts were touting their technology. By January 2015 it was up over 400%. Having done significant research, I believe the thinly traded small cap Tokai Pharmaceuticals Inc (NASDAQ:TKAI) is a stock that is significantly undervalued by investors and is a good investment for traders with both short and long term timelines. I will explain why the Phase 3 clinical trial of Tokai’s prostate cancer drug Galeterone is highly de-risked and why the drug is poised to take a significant chunk of the multi-billion dollar prostate cancer market. With nearly $100M in cash, a blockbuster drug in the pipeline entering Phase 3, full commercial rights and a measly $270M market cap, Tokai Pharmaceuticals is one of my top picks for a multi-bagger.

Why Galeterone is Poised for Success

It has long been known that the development and progression of prostate cancer depends on androgenic stimulation through the androgen receptor. Therefore, blocking androgen and its function is the main method in which prostate cancer is treated. Currently, the second generation androgen inhibitor prostate cancer market is dominated by Medivation’s Xtandi and Johnson and Johnson’s Zytiga which combined rake in over $3 billion annually. I’ve written numerous times suggesting investors buy Medivation based on its superiority over Zytiga and recent studies proving treatment should be moved further upstream replacing the old androgen inhibitor Casodex, which has little effectiveness. Although many patients respond to Xtandi and Zytiga the effect of treatment is often transient as patients relapse after developing resistance. Importantly, there is no cure for castration resistant prostate cancer. Doctors strive to keep patients on various treatments as long as possible and move on to the next option once resistance emerges. Unfortunately, once resistance has occurred for Xtandi or Zytiga there are little options left if the patient has already had chemotherapy.

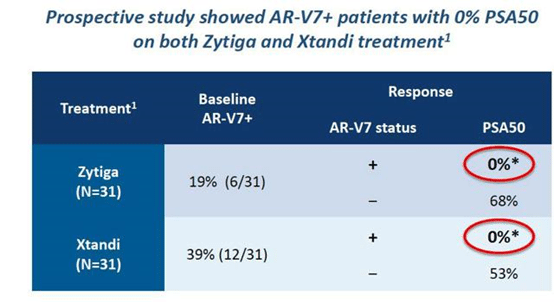

Resistance to androgen inhibitors can occur in treatment naïve patients or be acquired through exposure to drug. Numerous resistance mechanisms exist but strong evidence supports that a large percentage of patients are resistant due to mutations or expression of an AR isoform which disrupts the c-terminal of the protein which Xtandi and Zytiga need to function, keeping the AR active at all times. Thus, it makes sense that if patients are resistant to Xtandi they typically don’t respond to Zytiga and vice-versa. Multiple recent publications demonstrate that the presence of a truncated form of AR lacking the c-terminal called AR-V7 is a significant mechanism of resistance. In fact, numerous publications put the base-line AR-V7 expression at ~20% in treatment naïve patients so even before any Xtandi or Zytiga treatment. Following treatment, acquired resistance due to AR-V7 expression climbs to over 50%. Again, the AR-V7 protein lacks the domain needed for Xtandi and Zytiga to work and therefore they are ineffective. In accordance, a recent high-profile publication from Johns Hopkins in the New England Journal of Medicine showed in a prospective trial that prostate cancer patients expressing AR-V7 had a 0% PSA50 response rate when treated with either Xtandi or Zytiga.

*Slide from May 2015 Bank of America Merrill Lynch Health Care Conference

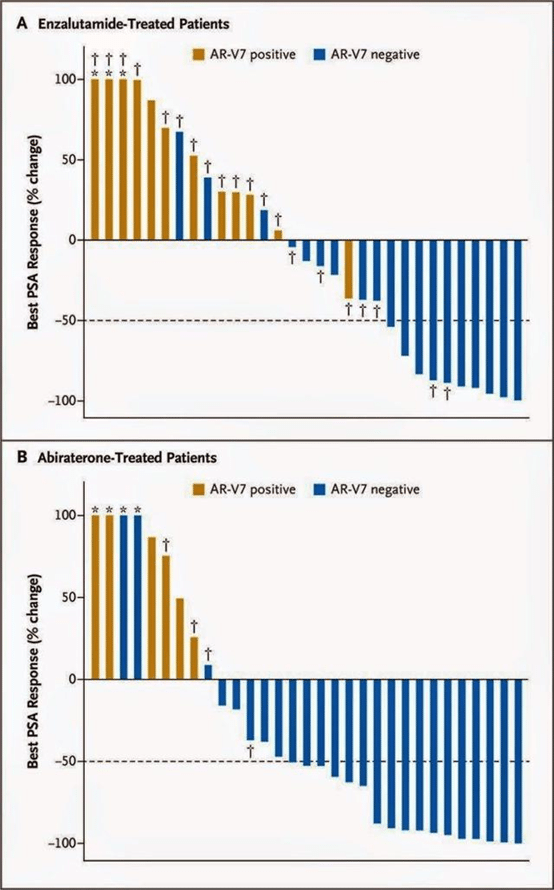

The data is extremely clear in the waterfall plot detailing AR-V7 positive and negative patients and their response to Xtandi and Zytiga.

*Figure from Antonarakis et al., 2014 NEJM paper

Retrospective studies conducted by MD Anderson and Memorial Sloan Kettering Cancer Centers confirm that AR-V7 expression is associated with extremely poor responsiveness to Xtandi and Zytiga. This is where Galeterone enters the picture.

Galeterone’s Mechanism of Action is a Game Changer

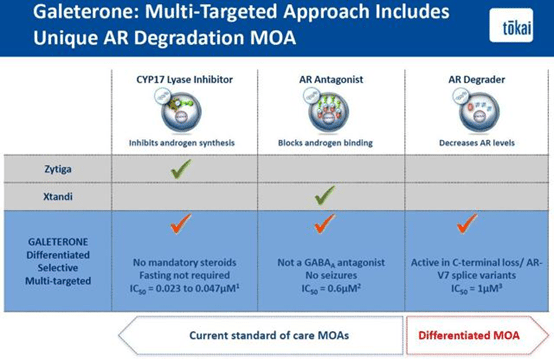

Galeterone has a unique mechanism of action that differentiates itself from all other androgen inhibitors on the market like Xtandi and Zytiga and even those currently in development like JNJ’s ARN-509. These drugs either block androgen synthesis by CYP17 Lyase inhibition like Zytiga or bind and block the AR itself like Xtandi and ARN-509. Obviously, neither is effective in patients expressing AR-V7 since the mutant receptor is active without any androgen binding. Multi-targeted Galeterone appears to be the best of all worlds. Galeterone is both a CYP17 Lyase inhibitor and an AR blocker. In addition, it doesn’t have the mandatory steroid and food restrictions of Zytiga or any evidence of seizures that has been observed in a very small subset of Xtandi treated patients. However, the reason Galeterone is a game-changer is because preclinical and clinical evidence shows that the drug also functions by actually degrading the AR. This activity enables the drug to be effective in treating patients with AR-V7 and other mutant forms of the AR where all other drugs fail.

*Slide from May 2015 Bank of America Merrill Lynch Health Care Conference

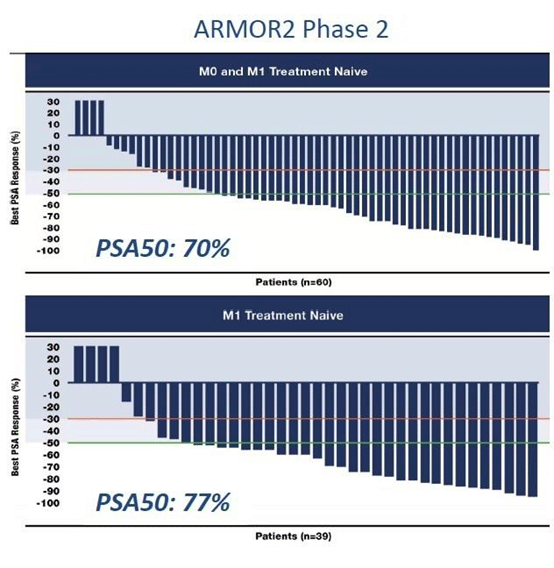

The 108 patient ARMOR2 trial was an open-label Phase 2 trial evaluating the safety and efficacy of Galeterone in treatment naïve patients with either non-metastatic or metastatic CRPC and in a subset of patients who had failed previous treatments with androgen inhibitors. The trial is still ongoing but the data released to date has been very impressive. The PSA50 response in both non-metastatic and metastatic CRPC patients is over 70% which puts Galeterone on par with Xtandi and Zytiga.

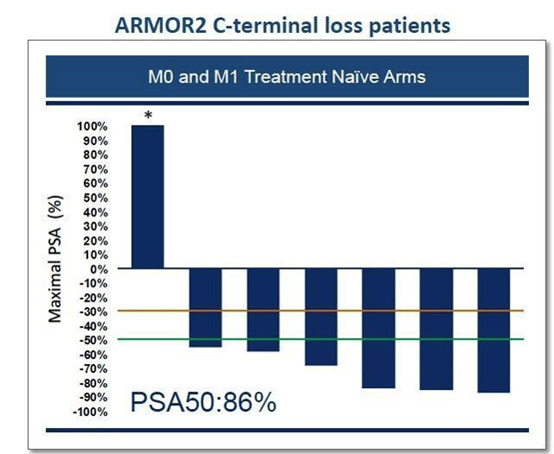

*Slide from May 2015 Bank of America Merrill Lynch Health Care Conference

However, what has caused the most excitement is when investigators went back to the data and looked at the responses of those patients where AR-V7 was tested for and detected. Incredibly, 6 of the 7 patients with AR-V7 or 86% had a PSA50 response.

The non-responder really should not be included as they discontinued treatment due to an unrelated adverse event only half-way through treatment. The median time to PSA progression in these patients was 7.3 months. Therefore, the AR degradation mechanism of Galeterone provides a unique advantage over other drugs on the market by being effective in those patients with c-terminal loss of the AR, such as AR-V7. With these results, Galeterone’s path to market just got a whole lot easier.

Phase 3 Trial Focusing on AR-V7 Patients Highly De-Risked

Management has announced that they will begin the ARMOR3-SV Phase 3 clinical trial in the second half of this year. The structure of the trial has been finalized and the FDA and EMA have both signed off on the design. The trial will enroll 148 patients with progressive metastatic CRPC with detectable AR-V7 expression. Patients will be randomized to treatment with either Galeterone or Xtandi. The primary endpoint is radiographic PFS (rPFS) with secondary endpoints of PSA response, OS, time to chemotherapy, and safety.

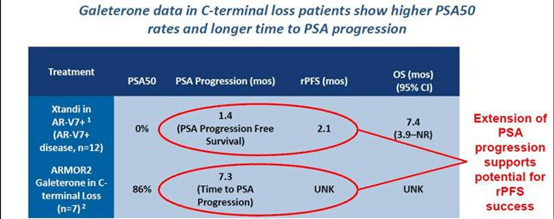

It’s hard to find a Phase 3 clinical trial as de-risked as the one set-up by Tokai management. In my opinion, the chance of success here is nearly 100%. Galeterone has been shown to be just as effective in patients with AR-V7 than without due to its numerous mechanisms of action while Xtandi is known to be ineffective in patients with AR-V7. The Johns Hopkins study showed that patients with AR-V7 expression had no PSA50 response, only 1.4 months of PSA progression free survival and 2.1 months of rPFS. In the Phase 2 Galeterone clinical trial 86% of patients with AR-V7 achieved PSA50 response translating to a 7.3 month PSA PFS.

*Slide from May 2015 Bank of America Merrill Lynch Health Care Conference

Basically, the trial is similar to treating patients with an active drug and a sugar pill as the placebo as Xtandi has minimal effect in this patient population.

Galeterone A Billion Dollar Drug

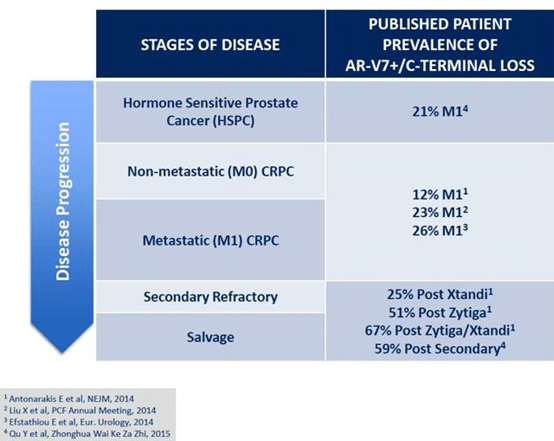

Make no mistake, the clinical data supports the use of Galeterone in the broader prostate cancer market to compete directly with Xtandi and Zytiga and those Phase 3 clinical trials are in development. However, by focusing on resistant patients at first, Galeterone can move to market relatively easy with zero competition. I have heard of no drug in any pipeline that is effective on AR-V7 patients. The main question is the size of the target population. The current Phase 3 trial is set-up to target those patients who have not been exposed to Xtandi or Zytiga but have expression of AR-V7. There have been four published publications which establish this population as 12-26% of metastatic CRPC patients.

*Slide from May 2015 Bank of America Merrill Lynch Health Care Conference

Therefore, if you estimate that the current market size for Xtandi and Zytiga is ~$3.5 Billion and that Galeterone would take ~20% of baseline resistant patients then ~$700M in annual revenue would be captured. As the prostate cancer market grows as is expected this number will get bigger. In my opinion, this is the worst case scenario for Galeterone. The big numbers come when you begin to take into account the percentage of patients who initially respond to Xtandi and Zytiga then become AR-V7 positive. The published literature puts those numbers at ~25-70% of patients. If those patients were started on Galeterone upon AR-V7 detection you’re theoretically looking at an additional $900 million to $2.5 billion annually. Remember this is all with just testing the resistant patients. In accordance, Oppenheimer put US peak sales at $1.4 billion by 2025 for the resistance indication alone. If approved for regular mCRPC and non-mCRPC, regardless of AR-V7 expression, these numbers become even bigger.

At Current Market Cap Tokai Pharmaceuticals is a Steal

Tokai Pharmaceuticals currently sits near its all-time low with a market cap of only ~$275M with over $90M of that in cash. The company is fairly new on Wall Street, going IPO less than a year ago at $15 per share. It promptly rocketed to $30 per share before recently settling back down below its IPO price this year. The stock is heavily shorted, making up nearly a quarter of traded shares, making a short squeeze highly likely to propel the stock higher. Tokai maintains the full commercial rights to Galeterone and very strong IP protection out to 2034. Although the company is well funded and is expected to have enough cash on hand to push the drug through Phase 3 topline results, Tokai makes one the best acquisition or partnership plays in biotech based on the drug’s unique mechanism of action and large potential market. Astellas, Medivation and Johnson and Johnson are obvious suitors but could also be a likely target for others trying to make up for lost revenue like Abbvie or get more into the cancer market like Gilead. For example, Johnson and Johnson acquired Argon Pharmaceuticals in 2013 for its prostate cancer drug candidate ARN-509 for $1 billion ($650M upfront and $350M in milestones). As discussed earlier, ARN-509 is very similar to Xtandi and would not be effective against AR-V7. This deal for a single mechanism androgen inhibitor with data not as impressive as Galeterone was for ~4 times the current market cap of Tokai.

Tokai Pharmaceuticals is heavily backed by Apple Tree Partners and Novartis Venture Funds. They have competent management and a strong board of directors, recently adding Cheryl Cohen who is the former Chief Commercial Operator of Medivation and David Kessler the former commissioner of the FDA. Currently, all 6 analysts who cover the stock rate the stock a strong buy with price targets ranging from $18-$44. Last month, Oppenheimer analyst Ling Wang listed a $38 12-18 month price target representing ~300% upside from current value. She predicted a 75% probability of success for the Phase 3 ARMOR2 trial. She summed it up perfectly stating:

“We view TKAI shares as having significant upside potential (phase III start 1H15, pivotal data 2H16), given a clear/favorable regulatory pathway, a high probability of phase III success, sizeable market opportunity (addressing a key resistance mechanism to novel therapies) and no foreseeable competition.”

Risks

Investing in small cap biotech stocks brings not only the potential for large rewards but also risk. The main risk for Tokai Pharmaceuticals is that Galeterone is their whole drug pipeline. Although managements has been very cautious in bringing Galeterone to market by focusing on the high unmet need of androgen inhibitor resistance there is always the possibility that the drug will not meet the endpoints for approval. Likewise, the ability of Galeterone to penetrate the market will rely on the establishment of the AR-V7 diagnostic assay. Tokai has recently partnered with Qiagen to commercialize the same assay used by the Johns Hopkins group in their study. However, Tokai will need to educate doctors to use the AR-V7 diagnostic assay before they can begin prescribing the drug.

Conclusion

Tokai Pharmaceuticals Galeterone addresses a huge unmet medical need in prostate cancer by targeting the high percentage of patients who are resistant to current androgen inhibitors Xtandi and Zytiga. To date, Galeterone is the only drug in development which has illustrated clinical activity against the AR-V7 variant expressed in patients with resistance. The Phase 3 ARMOR2 trial, beginning in the second half of this year, comparing Galeterone to Xtandi in AR-V7 expressing patients has a very high chance of success. Trading with a market cap of only $270M with nearly $100M in cash, I believe Tokai is extremely undervalued and a prime acquisition target for a pharma company looking to expand their cancer franchise. I expect the stock to double or triple in the next 6-12 months.